Similar concepts to depreciation, amortization and depletion are used by accountants to show how intangible assets and natural resources respectively are used up.

How it works

Amortization is how the cost of purchasing an intangible asset, such as copyright of an artwork, is spread over a period of time, usually its useful lifetime. It is shown as a reduction in the value of the intangible asset on the balance sheet and an expense on the income statement. In lending, amortization can also mean the paying off of debts over time. Depletion shows the exhaustion of natural resources such as coal mines, forests, or natural gas.

GOODWILL

In business, goodwill describes an intangible asset based on a company’s reputation, including loyal customers and suppliers, brand name, and public profile. Goodwill arises when one company buys another for more than its book value

(total assets minus total liabilities). For example, if Company A buys Company B for $10 million but the total sum of its assets and liabilities is $9 million, the goodwill is worth $1 million. According to International Financial Reporting Standards since 2001, goodwill does not amortize, so it does not appear as amortization in financial statements. However, if the value of goodwill falls (through negative publicity, for example) it can be recorded as an impairment.

NEED TO KNOW

- ❯ Intangible assets Nonphysical assets, such as patents, trademarks, brand recognition, and copyright; their valuation is sometimes subjective

- ❯ Patent A license granted by a government or authority giving the owner exclusive rights for making or owning an invention

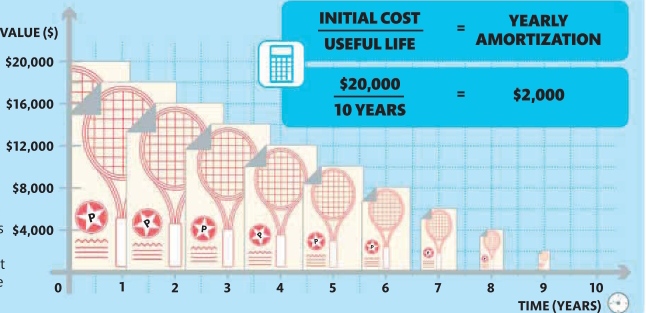

Amortization in practice

There are two types of amortization, one for spreading the cost of an intangible asset, the other for loan repayment. Both are calculated in similar ways, but loan repayments are worked out as a percentage.

Intangible assets

In this example, a company buys an intangible asset— a patent for a new, revolutionary type of tennis racket—for $20,000. The patent will be useful for 10 years, so its cost is recorded as a $2,000 amortization (expense) each year rather than as a one-time cost. Unlike tangible assets, a patent does not have a salvage value.

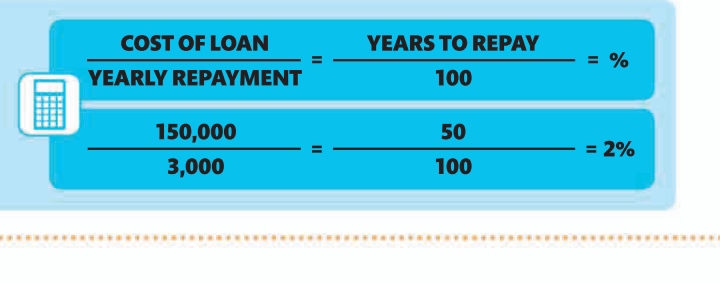

Loan percentage

If a company has an outstanding loan worth $150,000, and pays off $3,000 of this loan each year, then $3,000 of the loan has been amortized. It can also be said that 2 percent of the loan has been amortized, as it will take 50 years to repay the loan at this rate.

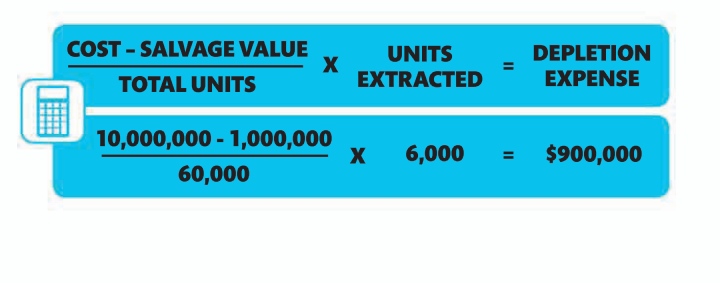

How to calculate depletion

Like amortization, depletion is calculated using the straight-line methods unless there is a particular reason to use another method.

In this example, a logging company buys a forest with an estimated 60,000 trees for $10 million. The original salvage value is $1.5 million, but the company spends $500,000 on road building in the forest, bringing it down to $1 million. The company cuts down 6,000 trees during each accounting period.