Capital gearing is the balance between the capital a company owns and its funding by short- or long-term loans. Investors and lenders use it to assess risk.

How it works

Most businesses operate on some form of gearing (also called financial leverage). They partly fund their operations by borrowing money, via loans and bonds, on the condition that they make regular repayments of a fixed amount to the lender. If the level of gearing is high (in other words, the business has taken on large debt), some investors will be concerned about its ability to repay and see this as an insolvency risk. However, if the amount of operating profit is more than enough to repay interest, high gearing can provide better returns to shareholders. The optimum level of gearing for a company also depends on how risky its business sector is, how heavily geared its competitors are, and what stage of its life cycle it is at.

Low gearing

Company has less debt

Company has more equity Low proportion of debt to equity, also described as a low degree of financial leverage. Equity comes from:

❯ Reserves (retained profits)

❯ Share capital

Equity finance (shares)

Pros

❯ Does not have to be repaid

❯ Shareholders absorb loss

❯ Good for start-ups, which may take a while to become profitable

❯ Angel investors share expertise

❯ Low gearing seen as a measure of financial strength

❯ Low risk attracts more investors and boosts credit rating

Cons

❯ Shared ownership, so company has limited control of decisions

❯ Shared profit in return for investors risking their funds ❯ Legal obligation to act in the interests of shareholders

❯ Heavy administrative load

❯Complex to set up

High gearing

Company has more debt

High proportion of debt to equity, also described as a high degree of financial leverage. Typical examples of debt are:

❯ Loans

❯ Bonds

Company has less equity

Debt finance (loans)

Pros

❯ If the company makes a profit, it can reap a larger proportion

❯ Paying interest is tax deductible

❯ Does not dilute ownership

❯ Company retains control of decisions

❯ Repayment is a known amount that can be planned for

❯ Quicker and simpler to set up

❯ Small business loans at favorable rates may be available to start-ups

Cons

❯ Loan must be repaid

❯ Interest must be paid, even if operating profit shrinks

❯ Debt may be secured on fixed assets of company

❯ Unpaid lender can seize assets and force bankruptcy

❯ Lenders first to be paid in the event of insolvency

❯ High gearing considered a measure of financial weakness

❯ High risk may put off investors and adversely affect credit rating

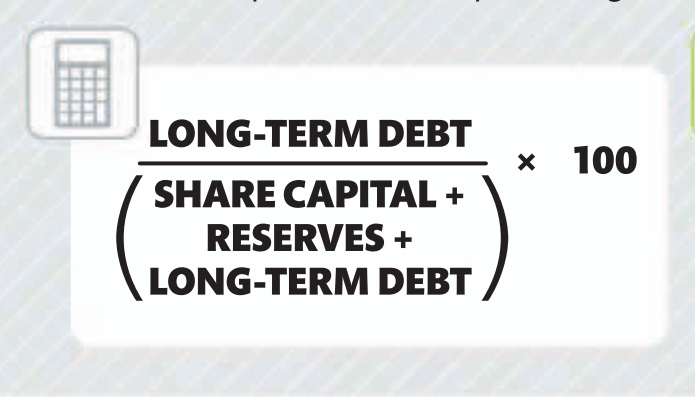

Gearing ratio calculation Analysts and potential investors assess the financial risk of a company with this calculation, presented as a percentage.

Low gearing A software company is going public. Its ratio of 21.2 percent tells investors that it has relatively low gearing and is well positioned to weather economic downturns.

High gearing A water utility is the only water provider in the area, with several million customers. The ratio of 64 percent is acceptable for a utility company with a regional monopoly and a good reputation.

NEED TO KNOW

❯ Interest cover ratio An alternative method of calculating gearing—operating profit divided by interest payable

❯ Overleveraged A situation in which a business has too much debt to meet interest payments on loans

❯ Deleverage Immediate payment of any existing debt in order to reduce gearing

The capital market is a global financial marketplace for trading long-term securities—bonds with a maturity of at least a year, and shares. It is where governments and businesses can raise funds and investors make money.

The structure

The capital market encompasses the debt capital market, where bonds are sold, and the stock exchange, where shares are sold. Both have a primary and a secondary market.

Capital market

Primary market

The market issues new bonds and shares, with investment banks overseeing the trading. It is also known as the new issue market (NIM).

GOVERNMENTS SELL BONDS

COMPANIES SELL BONDS AND SHARES

BONDS SHARES Sold on debt capital market (bond market)

SHARES Sold on debt capital market (bond market) Sold on stock exchange (equity capital marke

INVESTORS

Secondary market

Investors buy bonds and shares from other investors, not from issuing companies. The cash proceeds go to an investor, not to the underlying company or entity

BONDS

SHARES

Individual investors buy and sell shares and bonds previously issued on the primary market

WHAT IS A BOND?

A bond is a debt security that a company issues to investors. By buying bonds, an investor is effectively loaning money to the issuers, who in return agree to pay interest to the investor. A bond has a set term of maturity (a limited number of years of validity) and until that time the interest is paid to the investor annually. When the bond matures, the issuer repays the original sum of the loan to the investor. Companies or governments issue bonds to raise money that can then be put back into the business or used to fund government.

Bonds or shares: pros and cons

Bonds (debt investments)

✓Sellers are contractually obliged to pay interest✓Bonds are less risky: debt capital markets are less volatile than stock exchanges; if the issuing company has trouble, bondholders are paid before other expenses and before compensation to shareholders ✗ Buyers of bonds have no stake in the company

✗ Buyers cannot access principal sum until bonds mature

Shares (equity)

✓Buyers of shares gain a stake in the company

✓Sellers of shares have to pay dividends, although these can be reduced or suspended if the company feels it is necessary

✗ Shares are more risky: changes in company profits and in the economy as a whole can cause share prices to rise and fall; if the company fails, the shares become worthless

How do bonds work?

Bondholders effectively buy a slice of a larger loan with each bond, for which they receive interest, along with the original sum on maturity. Issuing, buying, and selling bonds takes place in the debt capital market. The marketplace has several functions: it offers bonds and other types of loans to investors; it operates as a fixedincome market, because the issuer is required to pay regular interest; and it enables companies and governments to raise long-term funds. Overall, the debt capital market is much larger than the stock exchange (equity capital market), where shares are bought and sold. It attracts investors because bonds provide more protection from risk than shares. There are various types of bonds, some safer than others—the risk lies in whether the issuer will be able to pay the interest and repay the principal sum on maturity. A secured bond is backed by an asset, such as property; an unsecured bond is not and so carries more risk. Both bonds and shares may be referred to as securities. The term describes the share or bond itself, and the certificate of ownership or creditorship that gives the holder the right to receive a dividend, in the case of shares, or interest payments, in the case of bonds.

TYPES OF BONDS

Government bonds are the safest type of bond since governments in developed capitalist economies are unlikely to default on interest payments on the loan or on the principal sum.

Corporate bonds

Secured bonds are secured by the assets of a company, making them a less risky investment than shares. Examples include equipment, trust certificates, and mortgage bonds

Unsecured bonds are not backed by pledged collateral and are a riskier investment—if the company fails, investors are paid only after secured bonds have been paid out. Because they are more risky, investors expect a higher return (interest) on their investment.

Investing in the debt capital market

A company wants to raise $100 million to finance growth but does not wish to issue further shares. Instead, it raises the money by issuing bonds on the debt capital market.

Company issues bonds The company issues 1 million bonds at $100 each. Each bond effectively acts as a loan between the investor and the company.

Investors buy bonds Each bond has a set maturity date of 10 years and a 7 percent interest rate, with a face value of $100. During the 10 years, the company can use the money as capital.

Investors receive annual interest Each year, the company pays an investor $7 (7 percent of $100) for each bond bought, in return for using the principal sum as capital to fund its business. After 10 years, the investor has received a total of $70 interest per bond.

Mature bond is repaid Once the bond reaches its date of maturity, in this case 10 years, the original sum of money, $100, is repaid to the investor. So the investor receives a total of $170, including interest, over the full term, in return for the original $100 investment.

NEED TO KNOW

❯ Debt instrument Official term for bond or other long-term debt

❯ Convertible bond Bond that can be converted into shares of the issuing company, or cash

❯ Warrant Security that allows the holder to buy stock in a company at a fixed price for a certain period of time

❯ Callable bond Bond that gives the issuer the right to redeem it before maturity

❯ Non-callable bond Bond that cannot be redeemed or sold back to the issuer before maturity but continues to provide interest

$100 trillion the estimated value of global debt markets

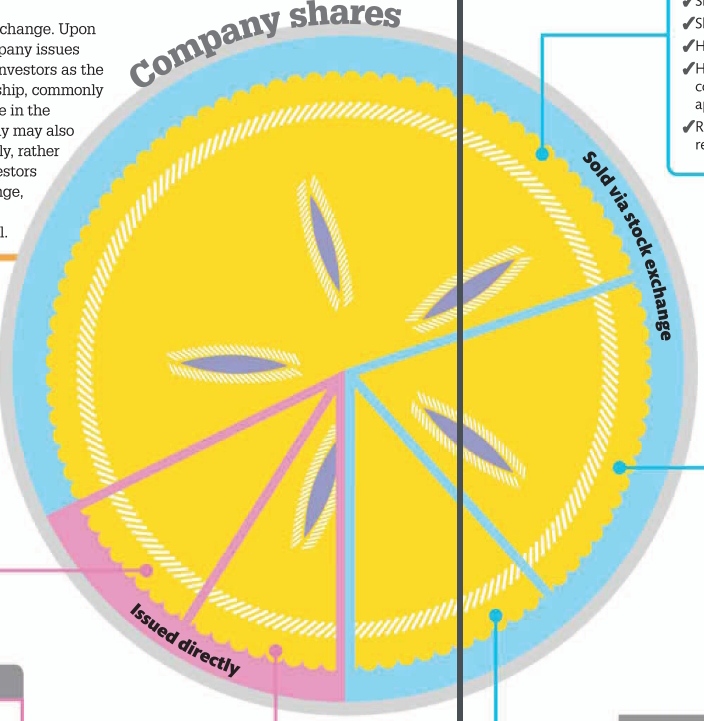

When a company goes public, it sells shares to investors, who become part-owners in return for capital investment. The number and type of shares bought by each investor determines the size of their ownership.

How it works

Before floating on a stock exchange, a company undergoes a valuation process to set the initial price of its shares. This process involves the directors, prospective investors, and an investment bank, which is appointed to assess the company’s value. Together, they reach a decision on the most financially viable price for the shares that will be offered on the exchange. Upon going public, a company issues ordinary shares to investors as the basic unit of ownership, commonly referred to as a stake in the business. A company may also issue shares privately, rather than publicly to investors via the stock exchange, to retain greater management control.

A share of the pie

Ordinary shares, issued by all companies when they go public, are the most common type of shares. There are also other share types, which give the company more flexibility to control rights available to different shareholder groups. Most shares are sold on the stock exchange, but non-voting and management shares are issued directly to holders. Different types of shares entitle the holder to different rights.

Company shares

Issued directly

Management shares Issued (usually given not sold) to owners and members of company management, who have:

✓Extra voting rights, so control of company stays in the same hands

Non-voting shares Issued to employees, who:

✓Receive a part of remuneration in the form of dividends

✗ Have no voting rights

✗ Receive no invitation to attend annual meeting

Solid bia stock exchange

Common stock Shareholders:

✓Share in the company dividends ✓Share in the company’s assets ✓Have right to attend AGM✓Have right to vote on important company matters such as appointment of directors

✓Receive the company’s annual report and financial statements

Preferred stock Shareholders:

✓Receive fixed dividend, paid ahead of any dividends paid out to ordinary shareholders✓Take priority in receiving a share of any assets left after debts are paid if company is insolvent

✗ Have fewer, if any, voting rights

RAISING MORE SHARE CAPITAL

After the initial sale of shares, when a company goes from private to public, the business can raise additional funds by issuing more shares. There are three main ways to do this:

❯ Rights issue entitles existing shareholders to buy additional shares from the company within a set time frame, before they are offered to other buyers.

❯ Public issue is a process by which the company issues a new allotment of shares to sell to the public on the stock market.

❯ Private placement is a practice by which the company sells its shares (or other securities) directly to private investors, usually large institutions, bypassing the stock exchange all together.

NEED TO KNOW

❯ Flipping Buying and quickly reselling IPOs for a large profit

❯ Redeemable shares Shares that may be later bought back by the issuing company for a cash sum

698% the increase in share price of IPO VA Linux Systems in one day on the New York Stock Exchange, in 1999

Establishing share value

The forces of supply and demand set the price of shares. Companies issue only a limited number of shares to the public, which can then be bought and sold on the stock exchange. Demand for those shares is determined by whether investors think the company has good future economic prospects. If investors believe that the company is primed for substantial growth, they will want to buy shares in it, which consequently drives up the share price.

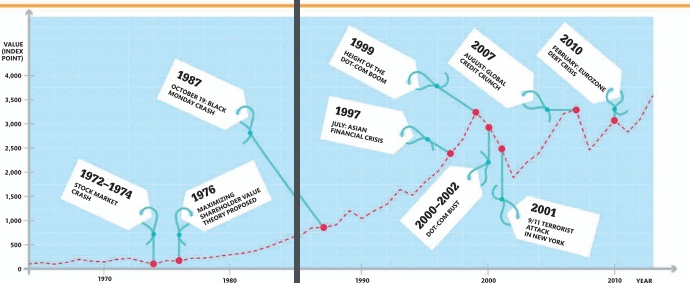

Rising value of shares

Financial market observers believe that the emphasis on optimizing the value of shares for shareholders began in 1976, when the idea of maximizing profit for shareholders became a priority. Since then, the market has experienced a general upward trend with occasional deep dips. The graph tracks the average value of all shares on London’s FTSE from 1964 to 2013.

SPLITTING SHARES

A company occasionally carries out a “share split” to its existing shares. This increases the total number of shares, although the combined value of shares stays the same. A share split allows a company to lower the price of its shares to bring them in line with the price of competitor shares. The share split is usually a two-for-one or three-for-one increase, whereby the shareholder sees the number of their shares double or triple.

SHARE PRICE TOO HIGH A company listed on the stock exchange has seen its share price increase so that its shares now cost more than its competitors’. The high price puts off investors.

SHARES SPLIT The company decides on a share split. It halves the price of each existing $3 share, so each share is now worth $1.50.

SHARE CERTIFICATES ISSUED It issues new share certificates to holders, doubling shares held: a shareholder with 1,000 shares at $3 each now has 2,000 at $1.50 each. Total worth is still $3,000.

SHARE VALUE ALIGNED The value of shares is now similar to that of competitors. The price encourages new investors to make a purchase.

NEED TO KNOW

❯ Bear market Market that has seen decline of 20 percent over a period of 2 months or more

❯ Bull market Market where share prices are rising and investor confidence is high

❯ Market correction Short-term decline in share prices to adjust for an overvaluation

25% the drop in share value over four days during the Wall Street Crash of 1929

What is a dividend?

Shareholders in a company are usually entitled to a payment of cash from its profits. The company pays a dividend sum on every share it has issued, but it is up to the company’s board to decide how much profit to reinvest and pay out. Investors may look at a company’s rate of dividend payout, along with its capital growth, to gauge its financial health and decide whether to invest in it. Investors who rely on shares for income are likely to invest in companies that reliably pay out dividends. In a good economic climate, they win twice—the dividend provides income and the capital value of the shareholding increases. However, there is always a risk that the value of shares will go down, and companies only pay dividends if they have made a profit. Paying dividends is a good way for a company to attract investors. It is essentially a reward for putting money into a company so that it can fund its existing output and develop and expand the business.

How it works

Shareholders usually receive a dividend if the company in which they hold shares has retained enough profit in that financial year to make the payment. The decision to make a payment is made by the board of directors. The dividend might be paid every quarter (four times a year), or in two parts—an interim dividend may be made partway through the year, with the final dividend paid just after the end of the financial year.

Announcing retained profits At the end of the financial year, the company announces its retained profits: the sum it intends to keep for reinvesting or paying off debts rather than pay out as dividends.

Making the decision for dividends The board of directors makes a decision on whether there is enough to warrant a dividend payment, and if so, how much. It records details of each payment in dividend vouchers.

Keeping funds for growth The company keeps some of its profit to put back into the business. It needs to strike a balance between pleasing investors and expanding its operation.

Making the payment Most dividends are cash dividends. Sometimes companies distribute stock dividends, issuing more shares instead of cash to shareholders.

Paying taxes Shareholders must declare dividends on their tax return and pay taxes on them.

INTEREST RATES AND DIVIDENDS

When interest rates are low, shares with high dividend payouts become extremely attractive to investors because they provide a better return than investments that yield an interest payment. This economic climate encourages companies to pay out top-rate dividends and so attract as many investors as possible, which in turn increases the share value. Conversely, when interest rates are rising, investors may prefer to put their money into fixed-income assets, which will pay high rates as a result of the hike without the risk attached to buying shares.

HIGH INTEREST RATES Investors are attracted to pay into fixed-income assets, such as deposit accounts.

LOW INTEREST RATES Investors are attracted to buy shares as dividends give a good return for their money.

NEED TO KNOW

❯ Dividend yield ratio Measure of how much a company pays out in dividends relative to the price of each share

❯ Dividend per share Sum paid on each share after retained profits have been calculated

❯ Dividend payout ratio Percentage of a company’s net income that is paid out in the form of dividends

1602 the year the Dutch East India Company became the first company to issue stocks and bonds

When a company changes from private to public, it offers shares for sale to members of the public. This process is known as going public and enables the company to raise money for growth.

How it works

The process by which an organization goes public (also known as flotation) marks the end of its life as a private company, after which it is no longer owned by a small number of shareholders or company members. A company may choose to go public when it needs capital to finance growth. Going public usually happens over several months; the company makes legal and financial preparations before the final stage, when it releases company shares for sale, either to selected investors or to the general public, or to a combination of both. Each share represents a “stake” in the company, and the money that the company receives from the sale of shares becomes capital, or wealth, which it now owns.

Ways to list on a stock exchange

There are three primary ways to take a company public, each of which has different associated costs. The type of public offering that a company chooses will be determined by its size and how much capital it needs to raise.

Introduction A company joins a new stock exchange without raising capital, but by trading its existing shares. To do this, over 25 percent of the shares must already be in public hands (on other stock exchanges) and no one shareholder can own a majority of shares.

Placing Select groups of institutional investors are invited to buy shares. This involves fewer costs than undertaking a full public share offering (see below) but the amount of capital that can potentially be raised is limited since there are fewer shareholders.

Initial Public Offering(IPO) Institutional and private investors are invited to subscribe to or buy from the first round of shares that the company issues. This is the most expensive way to go public, but allows for a company to raise large amounts of capital.

Stock exchange A financial market in which company securities (stocks and shares) are bought and sold according to current market rates.

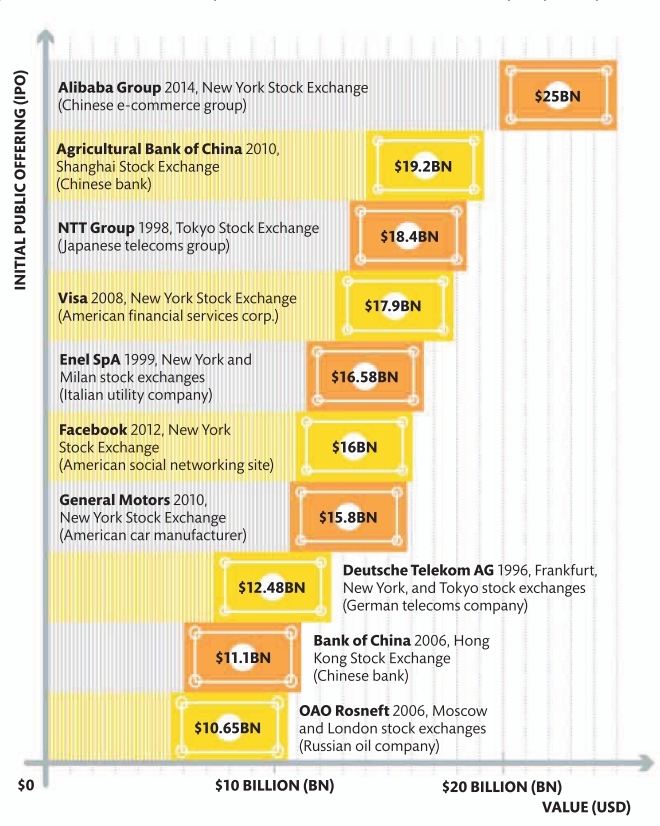

TEN LARGEST IPOS IN HISTORY

When a well-known private company undertakes an IPO, there is fierce competition between investors to buy its shares, and record-breaking activity can ensue. This graph shows the largest IPOs until 2014, based on proceeds from shares sold on the first day they went public.

WARNING

❯ Underestimation If the initial valuation of shares by the underwriters is too cautious, then the company will fail to realize the true value of its stock

❯ Overestimation If underwriters overestimate the value of shares newly on the market (new issue), it may flop due to lack of demand

❯ Volatility Share prices in the first few days of an IPO may fluctuate dramatically due to political or economic events

20%the typical minimum annual growth potential of public companies in the US

A closer look at IPOs

An Initial Public Offering (IPO) is the first time that shares in the company are offered for public sale. It is the most common way for a private company to go public if it needs a large injection of capital to fund major expansion. There are other reasons for going public—for example if a government wants to privatize a state-owned company, such as a national railroad, or if the members of a large family-owned enterprise want to sell their stake.

The IPO process

Before a company can issue shares, it has to be listed on a stock exchange where trading (the buying and selling of shares) can take place. The company must then fulfill the criteria necessary to secure investors. This process is lengthy, subject to strict financial regulations, and is extremely expensive to undertake. Only once all stages of the process are complete can the share offering be officially declared on a stock exchange.

1 Meet the qualifications The specific requirements are set by the stock exchange where the company plans to list. Listing conditions vary between exchanges, but typically demand:

Pretax earnings above a certain level

Three years of audited financial statements

Ability to pay the annual listing fee

1 Appoint underwriters These financial professionals will be responsible for buying and selling the shares to the public.

3 File a prospectus This document contains information about the offering, the business, and its financial history, and proposed plans. Details are still subject to change.

4 Promote the share offering Company representatives, as well as the underwriters, visit national and international destinations to pitch to potential investors.

5 Set the final offer price After ascertaining market conditions and the anticipated demand, the company decides the price and the number of shares to issue. It is then ready to launch the offering.

6 Sell on the stock market The IPO is officially declared a few days after potential investors receive the final prospectus. The declaration is made on a set day after the exchange has closed, and the shares are available for trading the following day.

NEED TO KNOW

❯ Large cap Listed company with market capitalization of more than $10 billion

❯ Mid cap Listed company with market capitalization of between $2 billion and $10 billion

❯ Small cap Listed company with market capitalization of between $250 million and $2 billion

$16.6 trillion the total market capitalization of companies listed on the New York Stock Exchange*

When business growth or unforeseen expenses cannot be met using internal sources of financing, such as retained profit, organizations must rely on finding funds from lenders or investors.

How it works

External financial support comes in various forms, including bank loans and issuing shares. The available sources of outside financing depend on the amount a company requires, and whether the money is needed to resolve a short-term issue, such as cash flow, or for the long-term growth of the business. While short-term financing is easier to secure, finding larger sums for an expansion is more challenging. A company that is either already listed on a stock exchange or is preparing to enlist will be able to raise the capital through the sale of shares. However, an unlisted company may struggle to raise a comparable amount. A company with a large amount of debt will also find it hard to raise funds, since lenders or investors will see the business as risky.

Raising external financing

Generating funds from external sources can be a challenge, especially when securing investors. However, revenue does not necessarily need to take the form of a loan. There are a number of strategies that can be implemented through working with external parties in order to provide a company with good working capital.

Short-term financing

A range of financial agreements that help provide a company with immediate funds can be made with outside parties as a way of raising cash short-term.

Bank line of credit Borrow from business checking account up to an agreed limit, with interest typically at a high rate.

Debt factoring Sell unpaid invoices to an external source for an agreed amount in order to receive immediate payment minus a commission fee.

Invoice discounting Borrow money against sales invoices customers are yet to pay (again, often at a disadvantageous rate).

Long-term financing

Putting effective measures in place to provide ongoing revenue is essential for a company’s long-term growth.

Shares Raise capital by issuing shares to finance growth. The company then retains less profit, as it pays dividends to shareholders, who also benefit from any capital gains in the company’s value

Borrowing Secure long-term loans from banks and other financial institutions, usually on better terms than a bank line of credit.

Finance leases Sell expensive assets such as computers to finance companies to release capital, and then lease them back.

Rent-to-own agreements Pay for expensive assets, such as vehicles, in installments. Overall cost may be higher, but capital is not tied up.

DEBT FACTORING PROCESS

To get money immediately, a company sells unpaid invoices (accounts receivable) to a third party, known as a “factor.” The factor advances the company a major portion of the amount, retains the rest until the account is paid, then charges a fee.

Company negotiates an agreement in which its unpaid receivables (invoices) are sold at a discount to a “factor.”

Company sends invoices out to customers, and copies these to the factor. Customer now owes payment to factor.

Factor pays company an agreed percentage of the invoices (typically 80–90 percent) within a few days of receipt.

Customer pays factor the invoice amount after 30 days (or more if terms of payment are longer).

Factor pays remaining invoice amount to company, minus a fee (usually 2–5 percent of the invoice amount).

NEED TO KNOW

❯ Term loan A bank debt repaid over a set period of time

❯ Loan note A form promising payment to the holder at an agreed future date

❯ Eurobond A bond issued in a currency other than the currency of the country in which it is issued

80% of external corporate financing is provided by domestic banks

Most companies prefer to secure funding from their own internal resources, rather than either take on debt through borrowing or give up a stake in the company by issuing shares, both of which cost more.

How it works

When a business needs funds, or capital, to pay for expansion or investment in order to maintain its current operations, it is faced with two choices: either find the money from outside sources, or find the money from within the organization itself. Since there are costs attached to bringing in funds from external sources, such as interest that has to be paid on a bank loan, the business managers must weigh up the opportunity cost of using its own funds—the profit it could earn by investing those funds—against the cost of financing.

Company

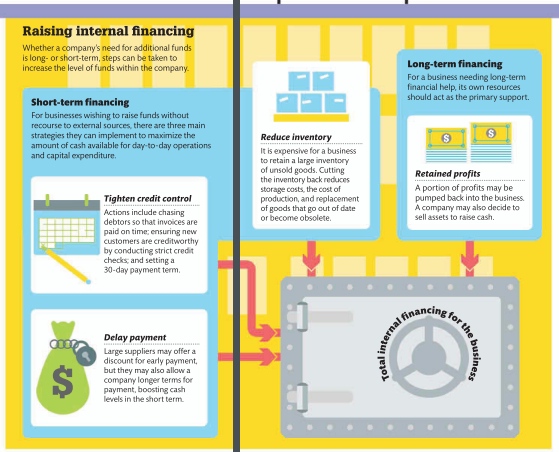

Raising internal financing

Whether a company’s need for additional funds is long- or short-term, steps can be taken to increase the level of funds within the company.

Short-term financing

For businesses wishing to raise funds without recourse to external sources, there are three main strategies they can implement to maximize the amount of cash available for day-to-day operations and capital expenditure.

Tighten credit control Actions include chasing debtors so that invoices are paid on time; ensuring new customers are creditworthy by conducting strict credit checks; and setting a 30-day payment term

Delay payment Large suppliers may offer a discount for early payment, but they may also allow a company longer terms for payment, boosting cash levels in the short term.

Reduce inventory It is expensive for a business to retain a large inventory of unsold goods. Cutting the inventory back reduces storage costs, the cost of production, and replacement of goods that go out of date or become obsolete.

Long-term financing

For a business needing long-term financial help, its own resources should act as the primary support.

Retained profits A portion of profits may be pumped back into the business. A company may also decide to sell assets to raise cash.

USING PROFITS TO FUND EXPANSION

A company seeking to grow may choose to fund the expansion with its profits. This option offers both advantages and disadvantages.

Pros

❯ The use of profits means that no interest payment has to be made, unlike on money that is borrowed

❯ Existing owners and directors are able to retain full control over the business, rather than sharing it with new investors

❯ The company is able to keep a low debt profile, which will appeal to future investors and lenders

Cons

❯ Profits can take time to build up sufficiently to fund expansion

❯ Withholding dividends may upset some shareholders who prefer to receive the profit as dividends

❯ Lost opportunity to earn funds from investing profit rather than spending it

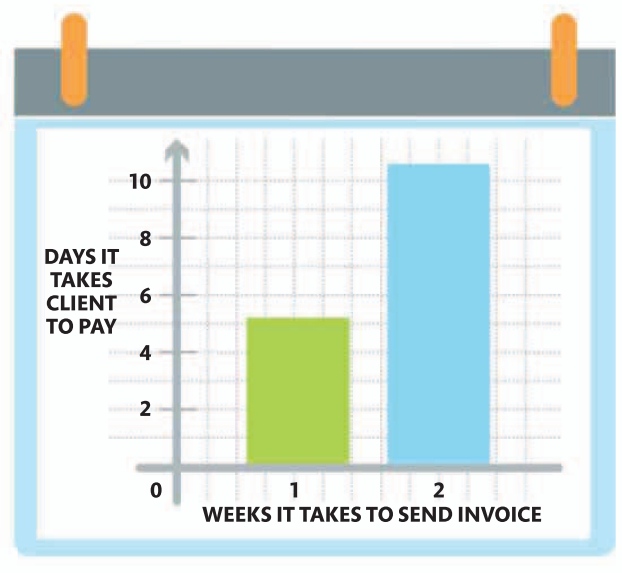

THE RECENCY BIAS

When a company receives timely payments for its invoices, this helps maintain its levels of funds. Interestingly, invoices issued right after completion of work tend to get paid sooner than those invoices that are sent later. A theory called recency bias explains this phenomenon: the brain prioritizes recent events over those that occurred longer ago.

44 the average number of days it takes a limited company in the UK to pay a 30-day invoice

When a company needs additional funds, it can use either internal or external sources, or both, depending on whether it seeks large amounts of funding for long-term growth, such as an expansion, or smaller amounts for short-term expenses, such as to cover operating costs. In addition, the number of external sources available depends on whether the business is well established or whether it is relatively new and without much of a track record.

Sources of financing and capital

When considering the prospect of raising financing, the financial directors will first evaluate the financial health of the company. They will then decide what proportion of the company will be funded by equity (the company’s own reserves of cash and money raised from issuing shares) and what proportion will be funded by borrowing money from an outside source, such as a bank, so that the company takes on debt.

EVALUATING CAPITAL STRUCTURE

When investors consider buying shares in a company, they look at its capital structure to assess the future prospects of the business. The capital structure refers to the percentage of a company’s finances made up of funds from shares and earnings, called equity, and the percentage made up from borrowed funds, or debt. When evaluating capital structure, investors consider the following:

❯ As a general rule, companies with more equity than debt are considered less risky to invest in because their assets outweigh their liabilities. So a company with significantly more equity than debt has a low debt-to-equity ratio and is generally seen to be a low-risk investment.

❯ A company with significantly more debt than equity has a high debt-to-equity ratio and is more risky as an investment.

❯ Debt is not always bad. If interest rates are low a company could take on more debt to fund expansion, as long as the revenue it makes from the borrowed funds is greater than the interest payable. So although this company may be more risky, it may also have greater potential for growth—this is known as “gearing.”

Debt and loans

Institutional lenders Money loaned by large financial bodies, such as banks.

FUNDS IN THE FORM OF A LOAN FROM AN OUTSIDE SOURCE

Equity

Profit from business activities Proceeds of the core business.

Shareholders’ stake in company Payment received for shares in the company.

DIVIDENDS—PAID ONLY WHEN A COMPANY MAKES ENOUGH PROFIT

Bonds

Investor lenders Payments made by bondholders.

59% of US financial managers say financial flexibility is the most important factor in deciding how much debt the company takes on

Lenders, investors, analysts, internal management, and other interested parties calculate financial ratios to decipher what financial statements are really saying about the state of a business.

How it works

Financial ratios are used to assess the financial standing of a business and identify any problem areas that might affect its future prospects. The process involves comparing two related items in the financial statement, such as net sales to net worth or net income to net sales, and using those ratios to measure the relative performance of the company. There are many different ratios to choose from, depending on the purpose—for example, whether the purpose is to measure the company’s ability to provide a good return to shareholders, its capacity to handle debt, or the efficiency with which it operates. The ratios can also be used to compare a business with its competitors or in comparison to specific benchmarks within the company to determine how consistent its financial results are.

Top financial ratios

These are some of the ratios most commonly used by people involved with assessing businesses. They are best considered comparatively and in the context of the economic climate. The ratios are for analyzing established companies, usually public ones with shares traded on the stock exchange—start-ups and small-tomedium enterprises generally do not have a full enough range of figures to provide any kind of reliable guide.

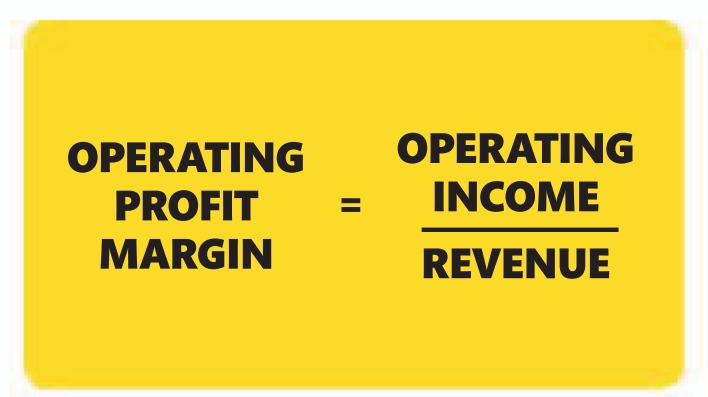

Profitability ratios

These are used to see how effective a company is at generating profit. Profitability ratios may mirror investment valuation ratios. One example is the operating profit margin ratio. A high ratio is good, as it indicates that a high proportion of revenue (gross income) converted into operating income (profit minus costs).

Other profitability ratios

❯ Return on equity (ROE) is measured as net income after tax / shareholders’ equity. The higher the ratio, the greater the profitability, but not if a company is relying too heavily on borrowing.

❯ EBITDA to sales ratio is measured as EBITDA (earnings before interest, taxes, depreciation, and amortization) / revenue. It gauges the profitability of core business operations. The higher the margin, the greater the profits.

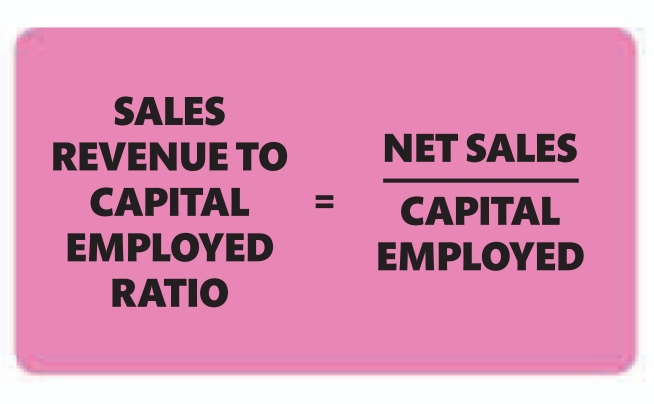

Efficiency ratios

These show how efficiently the company uses its assets and resources to maximize profits. An example is the sales revenue to capital employed ratio, which indicates a company’s ability to generate sales revenue by utilizing its assets. Similar ratios can examine how quickly the company settles its bills and invoices

Other efficiency ratios

❯ Accounts receivable turnover ratio is measured as net credit sales / average accounts receivable. It shows how efficiently a company turns sales into cash. The higher the ratio, the more frequently money is collected.

❯ Inventory turnover ratio is measured as the cost of goods sold / average inventory. It shows how efficiently a company manages its inventory level. A low ratio usually equates to poor sales.

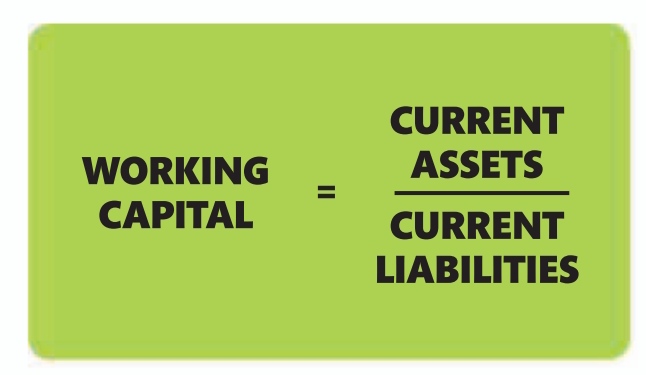

Liquidity ratios

This group of ratios reveals whether or not a company has enough cash or equivalent assets to meet its debt repayments. An example is the working capital ratio (also a measure of efficiency), which indicates whether a company has enough short-term assets to cover its short-term debt.

Other liquidity ratios

❯ Cash ratio is measured as total cash (and equivalents) / current liabilities. It shows whether a company’s shortterm assets could repay its debts. A high ratio is seen as favorable.

❯ Quick ratio (acid-test ratio) is measured as current assets minus inventories / current liabilities. It shows how easily a company can repay shortterm debt from cash. The higher the ratio, the more easily it can pay.

Solvency ratios

While liquidity ratios look at a company’s short-term ability to meet loan repayments, solvency ratios indicate the likelihood of a company being able to continue indefinitely with enough cash or current assets to pay its debts in the long run. An example is the debt to equity ratio.

Other solvency ratios

❯ Interest coverage ratio is measured as EBIT (earnings before interest and tax) / interest expense. It indicates how easily a company can pay the interest on its debts. The higher the ratio, the more easily they can pay.

❯ Debt ratio is measured as total liabilities / total assets. It indicates the percentage of the company’s assets that are financed by debt. A low ratio is considered favorable.

Investment valuation ratios

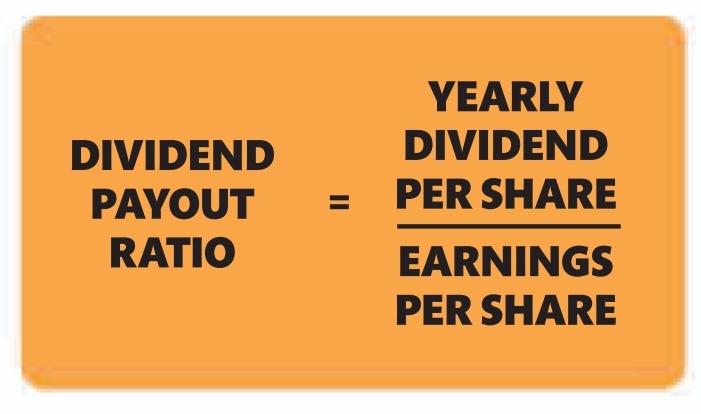

Thes ratios are typically used by investors to gauge the returns they are likely to get if they buy shares in a company. An example is the dividend payout ratio. It indicates how well earnings support the dividend payments—more mature companies tend to have a higher payout ratio.

Other investment valuation ratios

❯ Net profit margin ratio is measured as profit after tax / revenue. Another measure of a company’s profitability, it is also useful for comparing a company with competitors. The higher the ratio, the more profitable the company.

❯ Price to earnings ratio is measured as market value per share / earnings per share. It indicates the value of the company’s share price. A high ratio demonstrates good growth potential.

WARNING

Investors beware Ratio analysis must be used over time—at least four years—to understand how a company has reached its current position, not just what the position is. For instance, if debt has suddenly gone up, it could be because the company is branching out into new areas of potential profit, or to limit the damage of a poor past decision.

10–14% the minimum return on investment (ROI) needed to fund a company’s future

Knowing the full cost of creating each product that a business sells is vital because it helps a company price its products appropriately and assess the performance of the business.

How it works

Both direct and indirect costs contribute to the production cost of a product, whether it is a manufactured good or a service being provided. In order to calculate the cost of a product, it is treated as one unit of production. The direct and indirect costs involved in creating that single unit are then assessed and added together to create the full cost.

38% the average total of US business costs that can be accounted for by indirect costs

NEED TO KNOW

❯ Absorption costing Allocation of all production costs to product

❯ Differential costing Difference between the cost of two options ❯ Incremental (marginal) costing The change in total costs incurred when one additional unit is made ❯ Throughput costing An analysis of the impact that one extra unit of production will have on sales

❯ Cost-plus pricing Product price is based on direct and indirect costs, plus markup percentage

OTHER COSTING METHODS

There are several different approaches to costing and pricing depending on the industry, the type and size of the business, and the method of production.

JOB COSTING Used for a customized order made to a client’s specifications—for example, a printing company that prints brochures for a client

BATCH COSTING Used when a batch of identical products is made—for example, an electrical goods company manufacturing television sets

CONTRACT COSTING Used for a large one-time job, often the result of a tender process (when a company bids for work) and carried out at the client’s site—for example, a construction company building homes in a new residential development

PROCESS COSTING Used for an ongoing job that often involves several manufacturing processes, making it difficult to isolate individual unit costs—for example, an oil refinery which processes crude oil into diesel oil

SERVICE COSTING Used when the product being sold is a standard service offered to customers—for example, a nail salon offering an express manicure and pedicure within a set period of time and for a fixed price

Full cost pricing

Direct costs can be measured in terms of how materials and labor are used to produce each unit. Indirect costs (overheads) are harder to assess but also need to be factored in so that the full cost of each product can be calculated. Managers and accountants must apportion indirect costs to reflect their contribution to the cost of creating a single product. Once this is ascertained, the full cost of that product can be determined. In general terms, the price is worked out by adding the direct and indirect costs of production with a profit margin that gives an appropriate selling price.

Direct costs

❯ Materials

❯ Direct labor

❯ Direct expenses

❯ All used exclusively to create a product or service for sale

Share of indirect costs

❯ Production and service overheads❯ Administrative and management overheads

❯ Sales and distribution overheads

Profit margin

❯ Must be able to generate profit for the company

❯ Must be in line with how the product has been marketed

❯ Must be

pitched realistically so that customers will buy

Selling price

❯ Low: in order to gain market share, or to match competitors

❯ Cost-based: recover direct and indirect costs and profit margin that the market will accept

❯ Service-based: flexible since no manufacturing or distribution cost

Costs are the direct or indirect expenses that a business incurs in order to carry out activities that earn revenue, such as manufacturing goods or providing a service.

How it works

There are two main ways of classifying costs: direct, or variable, costs, which increase as more goods and services are sold, and indirect costs, which contribute to the overall running of the business and can either vary with the level of production or stay fixed. There are three main costs that businesses need to account for. The first is labor—wages paid to people employed to carry out a particular task. Labor can be regarded as direct or variable, or as a fixed cost or overhead. The second is the raw materials used in production and other materials used in service industries—these costs are variable. The third is expenses, which are other costs incurred in the course of the business’s activities.

NEED TO KNOW

❯ Break-even point (BEP) The point at which total sales revenue is equal to total costs

❯ Questionable costs Costs that can be treated as fixed or variable ❯ Sunk costs Costs incurred in the past that cannot be recovered

❯ Prospective costs Costs that may be incurred in the future depending on which business decisions are made

Fixed and variable costs

One way of looking at costs is to split them into two categories: fixed costs, which do not change with the level of business activity, and variable costs, which do change with the level of business activity. This helps accountants to determine how changes in business activity (for example, cutting or increasing production) will affect costs. In reality, some fixed costs will increase once business activity reaches a certain level—these are called stepped fixed costs.

Fixed costs

RENT AND INSURANCE COSTS

LAUNDRY SERVICES

STAFF SALARIES

CLEANING BILL

A restaurant rents premises to cater for 40 diners. The fixed costs are the same whether the restaurant serves 30 or 40 diners a night.

Stepped fixed costs

HIGHER RENT AND INSURANCE COSTS

EXTRA LAUNDRY SERVICES

HIGHER STAFF COSTS

HIGHER CLEANING BILL

The restaurant becomes popular, so the owner rents the premises next door to serve an additional 40 diners a night. The costs that were fixed at a certain level have now doubled.

Variable costs

The head chef orders the ingredients that will be required each day. For peak evenings the cost of the food order is higher; for quieter nights, the food order is lower.

LARGE FOOD ORDER

PEAK EVENINGS

QUIETER EVENINGS

SMALL FOOD ORDER

40% of business owners say that payroll is their greatest expense

A company’s possessions, or assets, are divided into two categories: fixed (or long-term) assets and current (or short-term) assets. Current assets consist of cash in the bank and inventory.

How it works

Fixed assets are items that enable a business to operate. They tend to be long-term holdings and cannot be easily converted into cash. Fixed assets can be categorized as either tangible or intangible: tangible assets are material objects, while intangible assets have no physical form.Current assets are held for the short term and used mainly for trading. The most important category in terms of generating revenue is current assets. The key component of these is inventory. Inventory can be finished goods ready for sale, but it can also be the raw materials that will be used for producing the goods.

NEED TO KNOW

❯ Asset valuation A method of assessing the value of a company’s holdings. Asset valuations may take place prior to a merger or the sale of the business, or for insurance purposes

TYPES OF INVENTORY

Inventory can include three types of stock, depending on the kind of business being carried out: raw materials, unfinished goods, and finished goods

Raw materials

Materials and components scheduled for use in making a product. For example, a chocolate factory will have:

❯ Ingredients in the form of sugar, cocoa mass, cocoa butter, additives, flavorings, and perhaps milk or nuts.

❯ Foil, plastic, and paper for the wrappers and packaging

Work in progress

Materials and components that have begun their transformation into finished goods; these may be referred to as “unfinished goods.” For instance, a graphic designer will have:

❯ Layouts and designs that are being developed and are awaiting client approval

Finished goods

The stock of completed products, or goods ready for sale to customers. A bookstore, for example, will have:

>Hardback and paperback books of various genres and formats supplied by publishing houses ❯ Gift items such as greeting cards and notebooks

Assets and inventory in practice

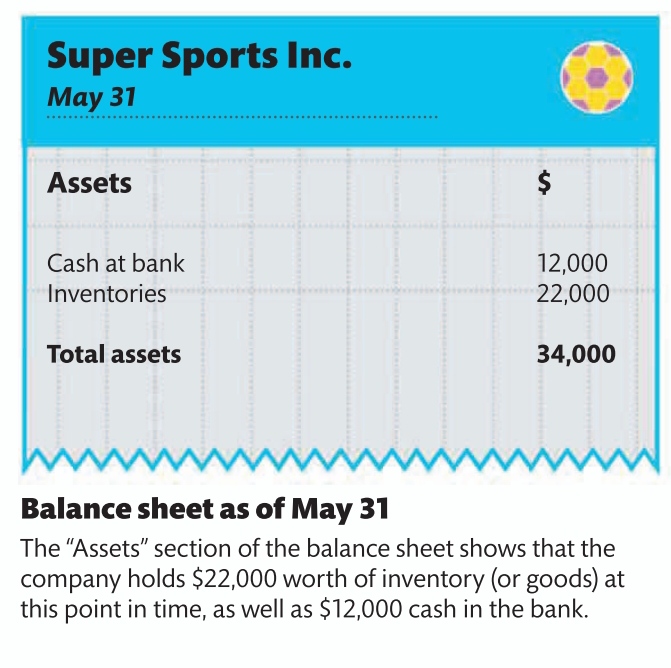

The partial balance sheets below show the current assets of a branch of Super Sports Inc., a sportswear and sports accessories company. These assets include cash in the bank and inventory held by the company. The inventory in this case consists of all the items in the shop that are ready for sale.

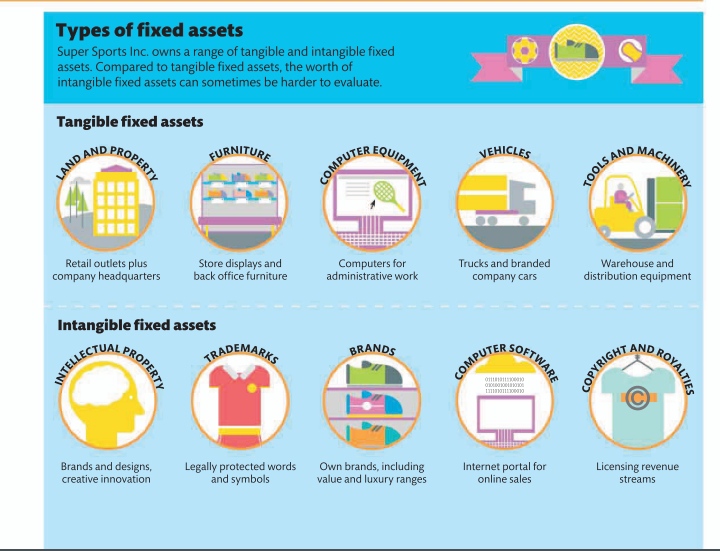

Types of fixed assets

Super Sports Inc. owns a range of tangible and intangible fixed assets. Compared to tangible fixed assets, the worth of intangible fixed assets can sometimes be harder to evaluate.

Setting the budget for a business involves planning the income and expenditure for the accounting year. This is usually broken down into months so that planned budget and actual figures can be compared.

How it works

Every business needs to budget for anticipated revenue and operating costs within the financial year. Unlike capital budgeting, in which senior management allocates what will be spent on specific projects or assets, revenue budgeting focuses on the overall projections for money coming in and money going out for each month of the coming financial, or accounting, year. Accountants compile operating budgets from each manager in the business, along with expected cash-flow projections for the business, to create a master budget. The master budget can also include figures for any financing that the company is expected to need over the coming year. As the year progresses, the projected budget and the actual money coming in and going out are monitored on a daily, weekly, or monthly basis, so that any deviations from the original budget can be identified, and, if necessary, remedied.

INCREMENTAL AND ZERO-BASED

There are two main approaches to setting budgets

Incremental budget

The budget for the year ahead is based on the previous year’s budget. This budget takes into account any changes, such as inflation, which could have an impact on the new calculations. The downside is that previous inaccuracies may be carried forward.

Zero-base budget

The coming year’s budget starts afresh, with no reference to previous years. This means that each item entered into the budget is carefully scrutinized and has to be justified by the department managers. This method makes it easier to see the full cost of all planned changes.

NEED TO KNOW

❯ Planning, Programming, and Budgeting Systems (PPBS) A budgeting system used in public service organizations such as city councils and hospitals ❯ Virement An amount saved under one cost heading in a budget is transferred to another cost heading to compensate for overspend ❯ Budget slack Deliberately underestimating sales or overestimating expenses in a budget

Setting and controlling budgets

Budget-setting is a process that takes place between the department managers, senior management, and finance department in a company to establish and control the cost of each department or project.

Consultation

Senior management sets out the company’s objectives to the departmental managers. Each manager is then responsible for working out the budget required by their individual department, in order to meet those objectives for the coming year.

Prepare the budget

The budget is usually based on the accounting year, but broken down into shorter periods. Departmental managers submit their budgets to senior management for approval. These may cover areas such as operating costs (salaries and supplies) and administration (office expenses).

Master budget

Once approved, the budgets from each department are combined into a master budget for the year, which includes: a budgeted profit-and-loss account, a projected balance sheet, and a budgeted cash-flow statement that typically shows a month-bymonth breakdown.

Measure performance

After each month (or equivalent time period set in the budget), the actual figures realized by the company are compared with the original budget projections. Variations are examined closely to work out whether they are significantly different from the figure in the original budget.

Take action

If necessary, the budget is revised to take into account any unforeseen and continued expenditure, or any savings that were not anticipated. If income is less than expected, action may be taken to alter departmental processes or campaigns in order to reach the targets set in the budget.

The money coming in and going out of a business is its cash flow; the balance of inflow and outflow is key to survival. Inflows arise from financing, operations, and investment, while outflows are expenses.

How it works

Cash flow is the movement of cash in and out of a business over a set period of time. Cash flows in from sales of goods and services, loans, capital investment, and other sources. Cash flows out to pay employees, rent and utilities, suppliers, and interest on loans. Timing is key—having enough cash coming in to pay bills on time keeps the company solvent.

Sales revenue

Cash for goods and services sold

❯ Revenue generated by core operation

❯ Basis of profit—does not have to be repaid, unlike loans or capital

❯ Company must be able to turn revenue into cash (get paid) to maintain cash flow

❯ Also known as cash flow from operating activities

Capital

Investment and lump sums

❯ Main source of cash inflow for start-ups

❯ Additional cash injection after initial start-up or at key stages in a company’s growt

❯Revenue from flotation of private companies (going public) and shares issued by public companies

❯ Also known as cash flow from investing activities

Loans

Bank loans and overdrafts

❯ Working capital loans to meet shortfalls, with anticipated inflows as collateral$ $CASH IN$ CASH OUT

❯ Advances on sales invoices from factoring companies

❯ Short-term overdrafts

❯ Also known as cash flow from financing activities

Other revenue

Grants, donations, and windfalls

❯ Grants from government or other institutions, usually one-time sums for research and development❯ Donations and gifts (applicable to nonprofit organizations)

❯ Sales of assets and investments

❯ Repayment of loans made to other organizations

❯ Tax refunds

“ Cash comes in, cash goes out, but the tank should never be empty.”

CASH OUT

Salaries and wages

Payments to employees

❯ Money paid to employees who are directly involved in the creation of goods or provision of services

❯ Salaries paid to staff as a fixed amount monthly or weekly (based on an annual rate)

❯ Wages paid to contractors for hours, days, or weeks worked

Overheads

Payment of bills

❯ Day-to-day running costs

❯ Rental cost of commercial property; utility bills—water, electricity, gas, telephone, and internet; office supplies and stationery

❯ Salaries and wages of employees not directly involved in creating goods and services (known as indirect labor)

Loan repayments

Debt servicing and shareholder profit

❯ Interest on long-term loans for asset purchases and on shortterm loans for working capital

❯ Repayments on capital loans

❯ Commission paid to factoring companies

❯ Cash distribution to shareholders via share repurchases and dividend payments

Suppliers

Payments for materials and services

❯ Cost of raw materials needed to manufacture goods for sale

❯ Cost of stock, imported or local

❯ Fees for services such as consulting or advertising to generate revenue

❯ Payments to contractors involved in goods and services creation

Tax

Payments to tax authorities

❯ Corporation tax based on annual financial statements

❯ Payroll tax paid by employers on behalf of employees

❯ Sales tax on goods or services

❯ Varies from country to country, depending on tax law

Equipment

Purchase of fixed assets

❯ Cost of buildings and equipment, such as computers and phones, office furniture, vehicles, plant, and machinery

❯ Offset by depreciation

Cash-flow management

The handling of cash flow determines the survival of any business. Equally important is a company’s ability to convert its earnings into cash, which is known as liquidity. No matter how profitable a business is, it may become insolvent if it cannot pay its bills on time. New businesses may become victims of their own success and fail through “insolvency by overtrading” if, for example, they spend too much on expansion before payments start coming in and run out of cash to pay debts and liabilities. In order to manage cash flow, it is essential for companies to forecast cash inflows and outflows. Sales predictions and cash conversion rates are important. A schedule of when payments are due from customers, and when a business has to pay its own wages, bills, suppliers, debts, and other costs, can help to predict shortfalls. If cash flow is mismanaged, a business may have to pay out before receiving payment, leading to cash shortages. Some businesses, such as supermarkets, receive stock on credit but are paid in cash, generating a cash surplus.

WARNING

Top five cash-flow problems

❯ Slow payment of invoices

❯ Credit terms on sales invoices set at 60 or 120 days, while credit terms on outgoings are 30 days

❯ Decline in sales due to change in economic climate or competition, or product becoming outmoded

❯ Underpriced product, especially in start-ups trying to compete

❯ Excessive outlay on payroll and overheads; buying rather than renting assets

NEED TO KNOW

❯ Factoring Transaction in which a business passes its invoices a third party (factor), which collects payment from the customer for a commission

❯ Accounts payable Payments a business has to make to others

❯ Accounts receivable Payments a business is due to receive

❯ Aging schedule A table charting accounts payable and accounts receivable according to their dates

❯ Cash-flow gap Interval between payments made and received

Cash conversion

Successful businesses convert their product or service into cash inflows before their bills are due. To make the conversion process more efficient, a business may speed up:

❯ Customer purchase ordering

❯ Order fulfillment and shipping

❯ Customer invoicing

❯ Accounts receivable collection period

❯ Payment and deposit

80% of small business start-ups across the world fail because of poor cash-flow management

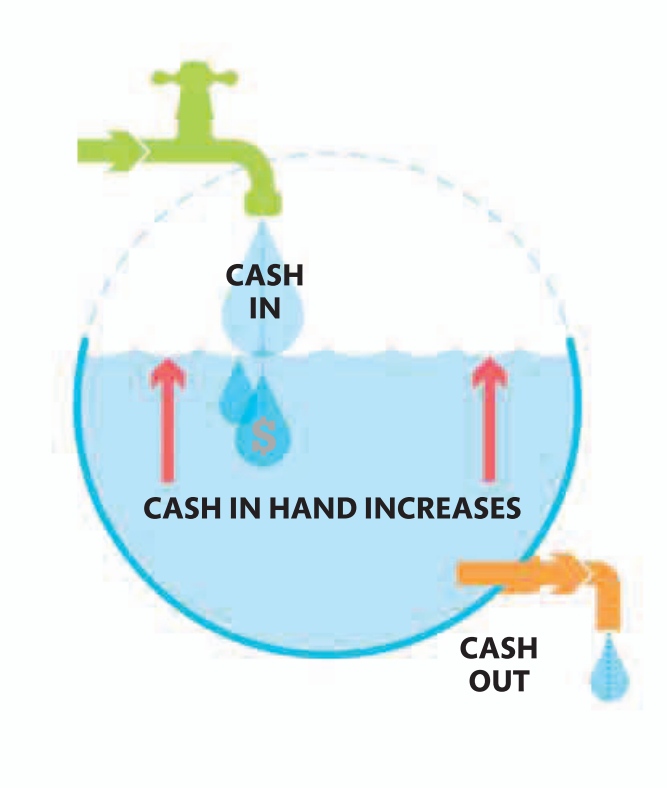

Positive and negative cash flow

Positive cash flow Cash flowing into the business is greater than cash flowing out. Cash in the tank—stock—increases. A business in this position is thriving.

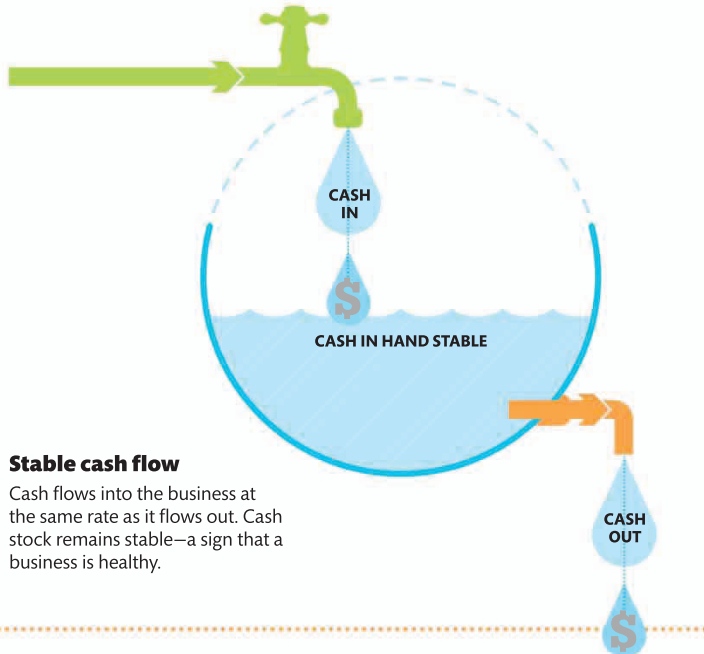

Stable cash flow Cash flows into the business at the same rate as it flows out. Cash stock remains stable—a sign that a business is healthy.

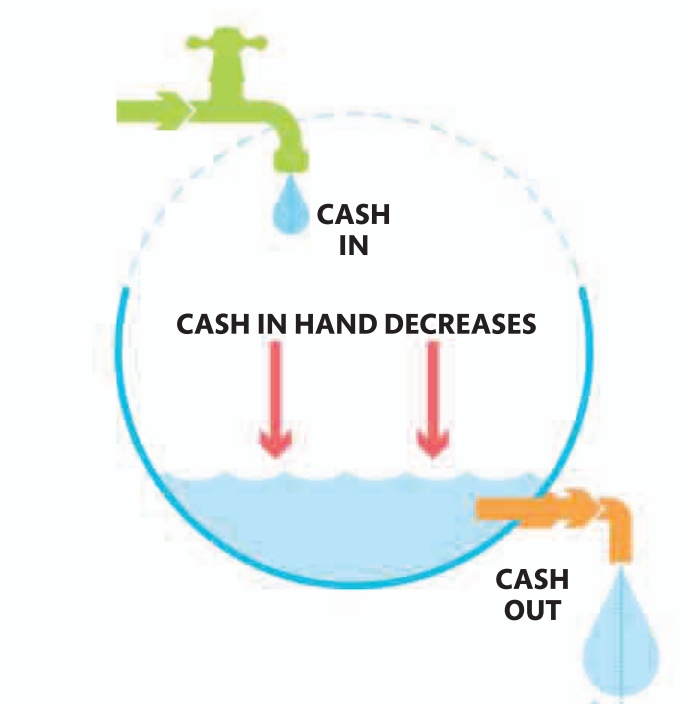

Negative cash flow Less cash is flowing into the business than is flowing out. Over time, the stock of cash will decrease and the business will face difficulties.

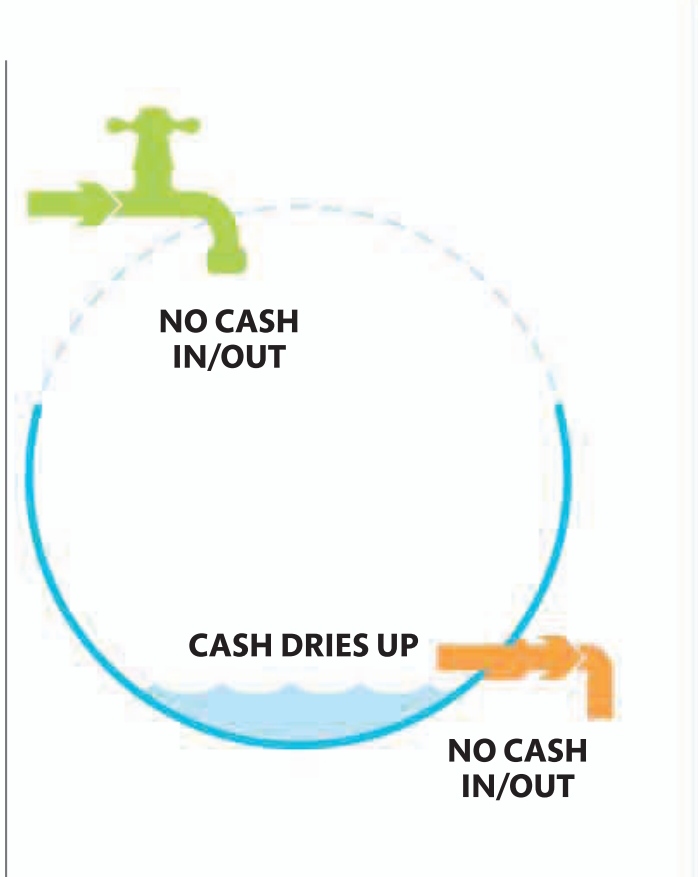

Bankruptcy If cash flowing out continues to exceed cash flowing in, cash stock levels will drop so low that the business becomes insolvent—it has no assets left to continue trading.

HANDLING THE FLOW

Managing a surplus

❯ Move excess cash into a bank account where it will earn interest, or make profitable investments.CASH IN CASH IN HAND DECREASES NO CASH IN/OUT

❯Use cash to upgrade equipment to improve production efficiency.

❯ Expand the business by taking on new staff, developing products, or buying other companies.

❯ Pay creditors early to improve credit credentials, or pay down debt before it is due.

Managing a shortage

❯ Increase sales by lowering prices, or profit margins by raising them.

❯ Issue invoices promptly and pursue overdue payments.

❯ Ask suppliers to extend credit.

❯Offer discounts on sales invoices in return for faster payment.

❯ Use an overdraft or short-term loan to pay off pressing expenses.

❯ Continue to forecast cash flow and plan to avert future problems.

For a company’s management to anticipate profit and loss, plan cash flow, and set effective goals for the business, the coming year’s incomings and outgoings need to be set out in detail. Unlike financial accounting, which is primarily for external users such as investors, lenders, or regulators, management or cost accounting takes place within a business to project expected sales revenue and expenses, so that the business can decide how to best use its available resources.

80% of accountants and financial professionals in the US are employed within a business or organization

COST ACCOUNTING PRINCIPLES

The Chartered Institute of Management Accounting (CIMA) in the UK and the American Institute of Certified Public Accountants (AICPA), with members in 177 countries, have established Global Management Accounting Principles.

❯ Communication provides insight that is influential Facilitate good decision-making through discussion.

❯ Information is relevant Source best material.

❯ Stewardship builds trust Protect financial and nonfinancial assets, reputation, and value of organization.

❯ Impact on value is analyzed Develop models to demonstrate outcomes in different scenarios.

Management accounting process

Planning is done for the financial (fiscal) year that lies ahead—this is also called the accounting year and is made up of 12 consecutive months. Start and end dates differ from country to country.

Department budgets Managers estimate what funds will be needed for expected outgoings

Purchase orders (POs) POs tell the finance department exactly how much money to reserve for payment.

Timesheets Staff employed on an hourly or daily basis fill in timesheets; these help managers to calculate overall staff costs

Invoices Invoices submitted by contractors and suppliers have to be matched against purchase orders and paid out.

Goods received Employees log receipt of merchandise, describing what the goods or services are and the quantity received.

Management

Managers create budgets and document business costs to monitor business performance, and plan for the short and medium term. The information they collate sheds light on the financial implications of ongoing projects

Information is passed to finance department

Finance department

Accountants in the finance department (or contracted from outside the business) receive information about the costs from managers. They then use these to generate reports and statements for the managers, who use this information to make decisions for the next financial year.

Profit-and-loss statement Also called an income statement, the P&L statement tells management how much money the business made or lost over a particular time period.

Balance sheet The balance sheet estimates the value of assets and inventory held, so that management can reduce it if necessary.

Cash-flow statement This shows how well the business will be able to meet its financial obligations and generate cash in the future.

Budget reports Reports help management to determine the accuracy of budgets and analyze business performance.

Cost of production report (CPR)CPR shows all of the costs that can be charged to a particular department

Similar concepts to depreciation, amortization and depletion are used by accountants to show how intangible assets and natural resources respectively are used up.

How it works

Amortization is how the cost of purchasing an intangible asset, such as copyright of an artwork, is spread over a period of time, usually its useful lifetime. It is shown as a reduction in the value of the intangible asset on the balance sheet and an expense on the income statement. In lending, amortization can also mean the paying off of debts over time. Depletion shows the exhaustion of natural resources such as coal mines, forests, or natural gas.

GOODWILL

In business, goodwill describes an intangible asset based on a company’s reputation, including loyal customers and suppliers, brand name, and public profile. Goodwill arises when one company buys another for more than its book value (total assets minus total liabilities). For example, if Company A buys Company B for $10 million but the total sum of its assets and liabilities is $9 million, the goodwill is worth $1 million. According to International Financial Reporting Standards since 2001, goodwill does not amortize, so it does not appear as amortization in financial statements. However, if the value of goodwill falls (through negative publicity, for example) it can be recorded as an impairment.

NEED TO KNOW

❯ Intangible assets Nonphysical assets, such as patents, trademarks, brand recognition, and copyright; their valuation is sometimes subjective

❯ Patent A license granted by a government or authority giving the owner exclusive rights for making or owning an invention

Amortization in practice

There are two types of amortization, one for spreading the cost of an intangible asset, the other for loan repayment. Both are calculated in similar ways, but loan repayments are worked out as a percentage.

Intangible assets

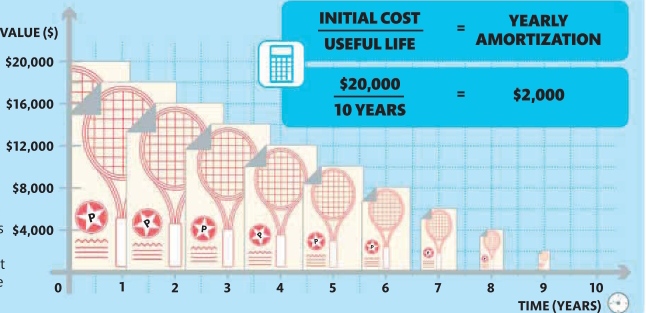

In this example, a company buys an intangible asset— a patent for a new, revolutionary type of tennis racket—for $20,000. The patent will be useful for 10 years, so its cost is recorded as a $2,000 amortization (expense) each year rather than as a one-time cost. Unlike tangible assets, a patent does not have a salvage value.

Loan percentage

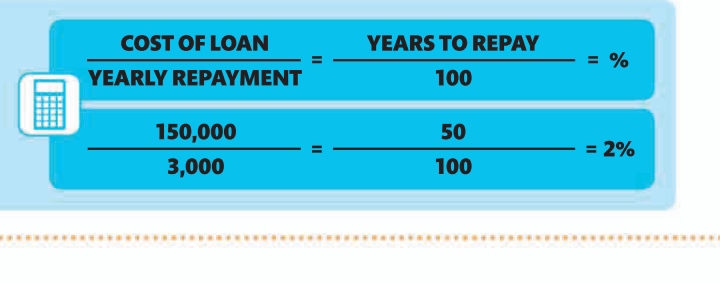

If a company has an outstanding loan worth $150,000, and pays off $3,000 of this loan each year, then $3,000 of the loan has been amortized. It can also be said that 2 percent of the loan has been amortized, as it will take 50 years to repay the loan at this rate.

How to calculate depletion

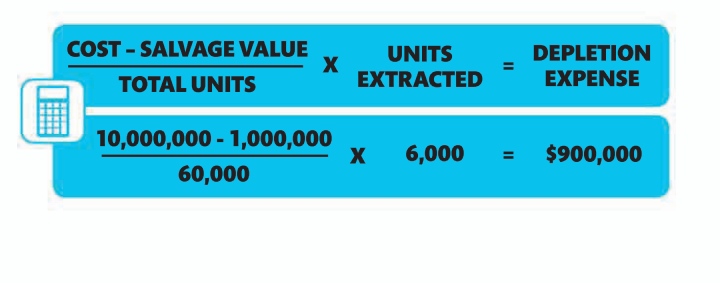

Like amortization, depletion is calculated using the straight-line methods unless there is a particular reason to use another method.

In this example, a logging company buys a forest with an estimated 60,000 trees for $10 million. The original salvage value is $1.5 million, but the company spends $500,000 on road building in the forest, bringing it down to $1 million. The company cuts down 6,000 trees during each accounting period.

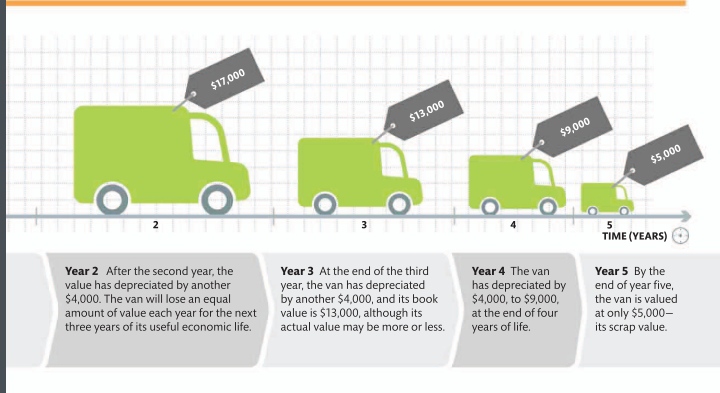

When a company buys an asset, its cost can be deducted from income for accounting and tax purposes. Depreciation allows the company to spread the cost, by calculating the asset’s decline in value over time.

How it works

If a business buys a long-lived asset, such as a building, factory equipment, or computer, to help it earn income, this expenditure can be offset as a cost against income earned. However, not all this income will be generated in the year of purchase and, over time, the asset will age and become less beneficial to the business, until it becomes outdated or unusable. Accountants do two things to turn the declining value into a tax advantage. Firstly, they work out how much the asset’s value decreases over a period of time—typically a year. Secondly, they match that loss in value to the amount of income earned in that period, so depreciation becomes a deduction from taxable income. There are several different ways to calculate depreciation. The method a company uses may depend on the kind of business, the type of asset, tax rules, or personal preference. In the United States, per IRS guidelines, companies must use MACRS (Modified Accelerated Cost Recovery System), a combination of straight-line and double declining balance methods.

NEED TO KNOW

❯ Fixed/tangible assets Items that enable a business to operate but are not a part of trade; assets lasting a year or more qualify for depreciation

❯ Useful/economic life Length of time an asset is fit for its purpose and has monetary value

❯ Salvage/scrap/residual value Worth of an asset once it has outlived its useful life—often set by the tax authority

❯ Book value An asset’s worth on

paper at any point between its initial purchase and salvage

TYPICAL LIFE OF FIXED ASSETS

Tax authorities often specify the typical useful (economic) life of a particular asset. This helps to standardize depreciation, and to eliminate uncertainty about value and the number of years over which an asset can be depreciated.

60%

the value the average car loses after three years

Calculating depreciation

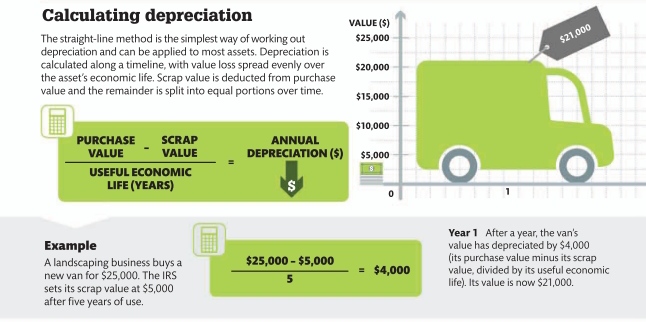

The straight-line method is the simplest way of working out depreciation and can be applied to most assets. Depreciation is calculated along a timeline, with value loss spread evenly over the asset’s economic life. Scrap value is deducted from purchase value and the remainder is split into equal portions over time.

Applying depreciation

When calculating depreciation, there are a number of different factors to consider. For instance, a business needs to be able to predict the number of years an asset will last. Helpfully, tax authorities in most countries issue guidelines to accountants and businesses with estimates of the useful economic life of many common business assets. Companies may also wonder which of the many methods of calculating depreciation to use for a given asset. Each method reflects a different pattern of depreciation, with some being more suitable for particular categories of assets. For example, the “accelerated” methods that chart rapid depreciation at the beginning of an asset’s life are more suitable for technology, while the “activity” methods that link depreciation to actual hours of use or number of units produced are best suited to transport and production lines. Again, tax authorities in most countries offer guidelines on which method to use. Although it is technically possible for a company to use two different methods for their own accounting and for tax purposes, this is best avoided.

WARNING

Misusing depreciation

❯ The wrong method A company must choose a method that is permissible for an asset type

❯ Frontloading Opting for an accelerated method can result in a taxable gain if an asset is sold early, for more than its book value

❯ Claiming beyond useful life Depreciation cannot be claimed after an asset’s useful life

❯ Ignoring depreciation If a company fails to claim depreciation, it has to report a gain from the sale, despite the loss on deduction

Other depreciation methods

There are many different methods of calculating depreciation. Some are favored by particular tax codes, while others are specifically applicable to certain industries and types of assets, and their patterns of value loss.

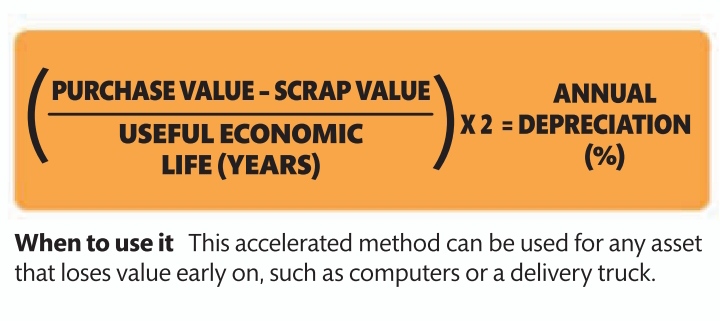

Double declining balance method

A method used to claim more depreciation in the first years after purchase, which is useful for assets that lose most of their value early on. It reduces a company’s net income in the early years of an asset’s life, but generates initial tax savings.

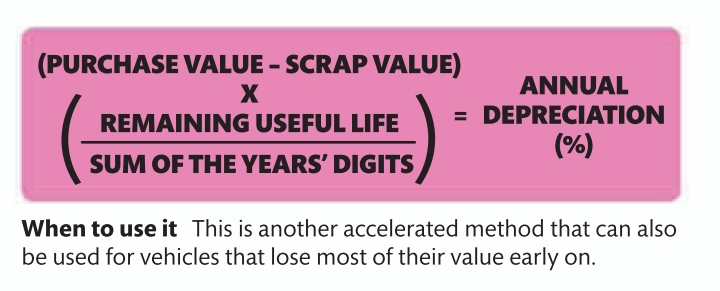

Sum of the years’ digits method (SYD)

Depreciation is calculated by dividing each year of the asset’s life by the sum of the total years to give a percentage of the depreciable value. If the asset’s useful life is 5 years, then the sum of the years as digits is 15 (5 + 4 + 3 + 2 + 1). In year 1, it loses 33 percent (5 ÷ 15), in year 2, 27 percent (4 ÷ 15), and so on.

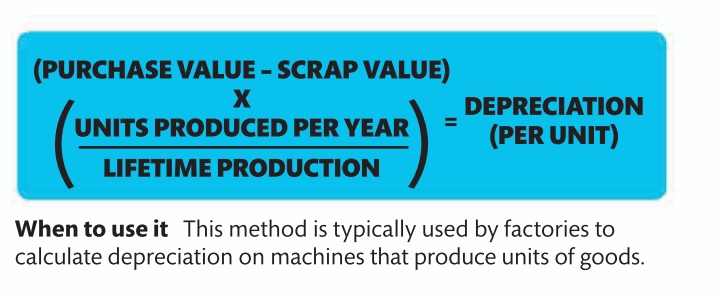

Units of production method

When a company uses an asset to produce quantifiable units, such as pages printed by a photocopier, it can claim depreciation with this method, which calculates depreciation according to the number of units an asset produces in a year.

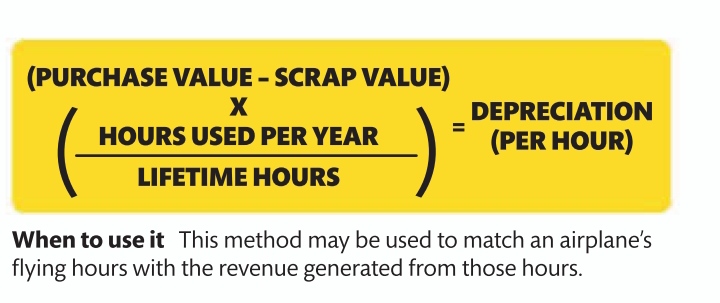

Hours of service method

The asset’s decline in value is measured according to the number of actual hours it is in use. To calculate depreciation using this method, the company measures the hours of use per year as a percentage of the estimated total lifetime hours. It is particularly useful for transportation industries.

Environmental regulations force companies to consider the impact of their activities and to adopt corporate social responsibility (CSR) as they grapple with legislation, climate change, and public opinion.

How it works

Globally, there are reams of different environment acts spread across multiple jurisdictions that affect the companies operating within their borders in different ways. Areas protected by environment acts include the atmosphere, fresh water, the marine environment, nature conservation, nuclear safety, and noise pollution. International acts are usually ratified by each country individually before taking effect there. An example of a common global means of reducing greenhouse gas emissions is emissions trading (“cap and trade”), by which companies must buy a permit for each ton of CO2 they emit over a certain level. Those emitting under the agreed level can sell their permits to other companies.

Environmental credentials

Most companies include a section on environmental accounting in their financial statement. Some details are required by law, but the statement also gives an opportunity to showcase environmental credentials to stakeholders.

Product responsibility

❯ Life-cycle stages in which the health-and-safety impact of products and services are assessed for improvement

❯ Adherence to laws, standards, and voluntary

codes relating to marketing communications

Society

❯ Programs and practices that assess and manage the impact of operations on communities

❯ Fines and sanctions for noncompliance with regulations

Economic

❯ Financial implications, risks, and opportunities for the organization’s activities due to climate change

❯ Financial assistance received from the government

Human rights

❯ Investment agreements that include human right clauses or that have undergone human rights screening

❯ Suppliers and contractors that have undergone screening on human rights; actions taken to address any issues

Labor practices

❯ Workforce by employment type, contract, and region

❯ Average hours of training per year, per employee by employee category

❯ Ratio of basic salary of men to women by employment category

GREENHOUSE GAS EMISSIONS

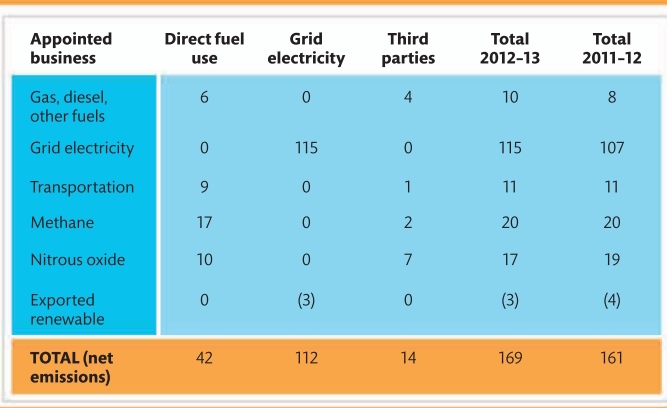

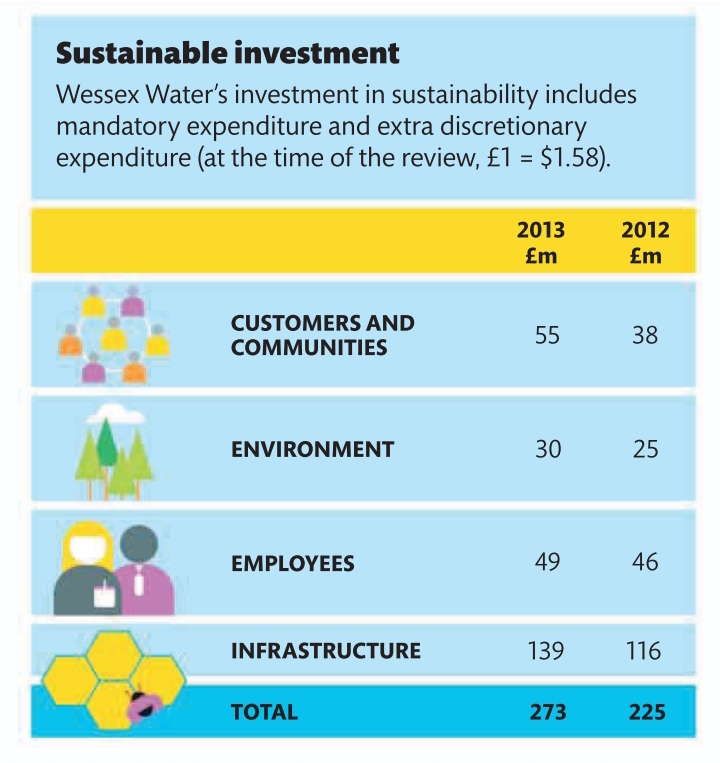

In some countries, companies are required by law to provide details of their greenhouse gas emissions. This is usually presented as a table in the environmental accounting section of the annual report. It includes direct and indirect emissions—by the company itself and by third parties—of gas, diesel, and other fuels; sulfur oxides and nitrous oxides; methane; and other ozonedepleting substances. In this table, from the Wessex Water utility company, emissions are shown as ktCO2 equivalents.

CASE STUDY

Cleaning up rivers

Wessex Water’s impressive record on pollution is mentioned several times in its statement, including in the chairman’s introduction. This prominence shows that the company believes acting in an environmentally conscious manner is important to its investors. The company illustrates several areas where it has acted with others to positively affect the environment:

❯ Work with the charity Surfers Against Sewage, which campaigns for clean seawater

❯ Its river strategy: collaborating with pressure groups and organizations to reduce pollutants and the impact of habitat alteration, and so increase the numbers of aquatic plants, invertebrates, and fish in local rivers

❯ Improving water quality at swimming beaches in the region, in compliance with mandatory standards

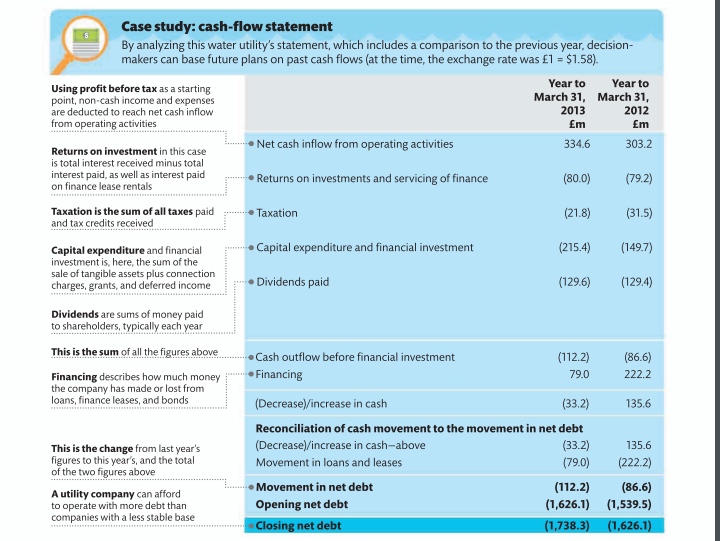

The cash-flow statement shows the movement of cash during the last accounting period. It is important because it reveals a company’s liquidity—whether or not it has more money coming in than going out.

How it works The cash-flow statement is often more useful for investors assessing a business’s health than other key statements, because it shows how the core activities are performing. The profit-and-loss statement, for example, obscures this by adding in non-cash factors such as depreciation. Similarly, the balance sheet is more concerned with assets than liquidity.

How to read a cash-flow statement

The statement of cash flows, to give it its official title, answers the key question of whether a business is making enough money to sustain itself and provide surplus capital to grow in the future, pay any debts, and give out dividends. Figures in parentheses are negative numbers.

Case study: cash-flow statement

By analyzing this water utility’s statement, which includes a comparison to the previous year, decisionmakers can base future plans on past cash flows (at the time, the exchange rate was £1 = $1.58).

Three types of cash flow

Cash refers to actual money as well as cash equivalents including cash in the bank; bank lines of credit, and short-term, highly liquid investments for which there is little risk of a change in value. Cash does not include interest, depreciation, or bad debts (debts written off).

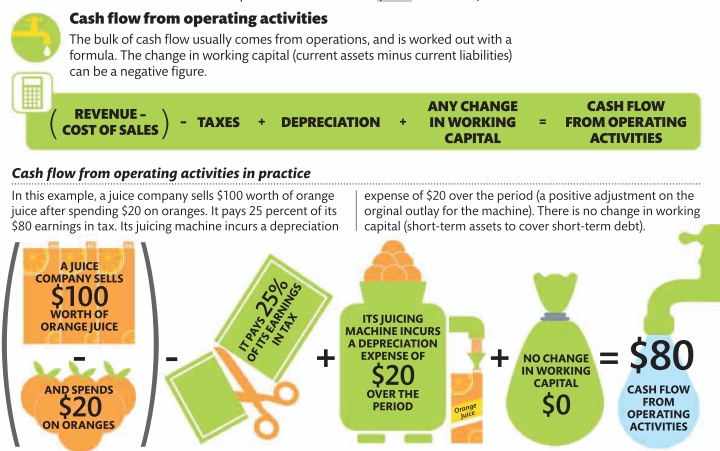

Cash flow from operating activities

The bulk of cash flow usually comes from operations, and is worked out with a formula. The change in working capital (current assets minus current liabilities) can be a negative figure.

Cash flow from investing activities

Buying or selling assets or investments is in this category. This figure is usually a cash outflow (negative figure) due to buying more than selling, but can be positive if there are significant sales.

Cash flow from financing activities

This includes buying or selling stock or debt and paying out dividends. Money made from selling something is called cash inflow; money lost through paying out is cash outflow.

Total cash flow

Adding all three cash flows gives the total. Separating out the three types shows decisionmakers the health of core activities as opposed to financing and investing, which bear little relation to day-to-day operations.

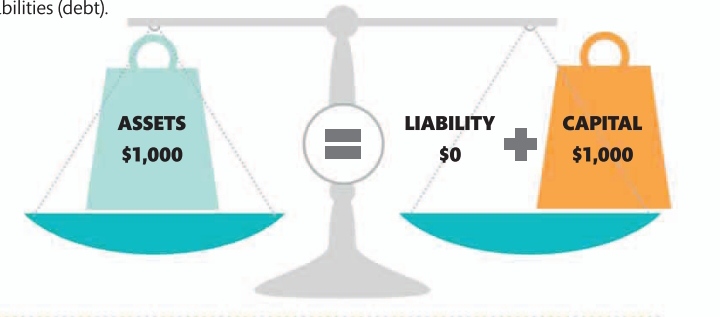

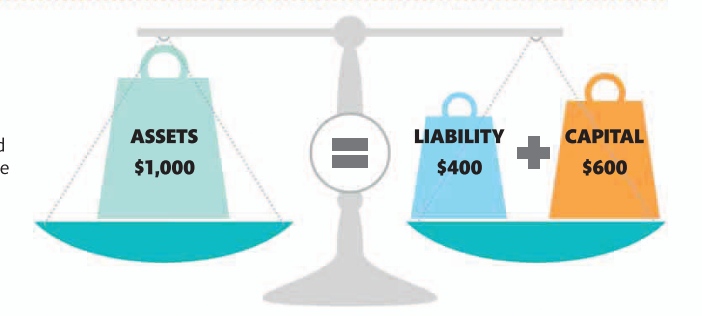

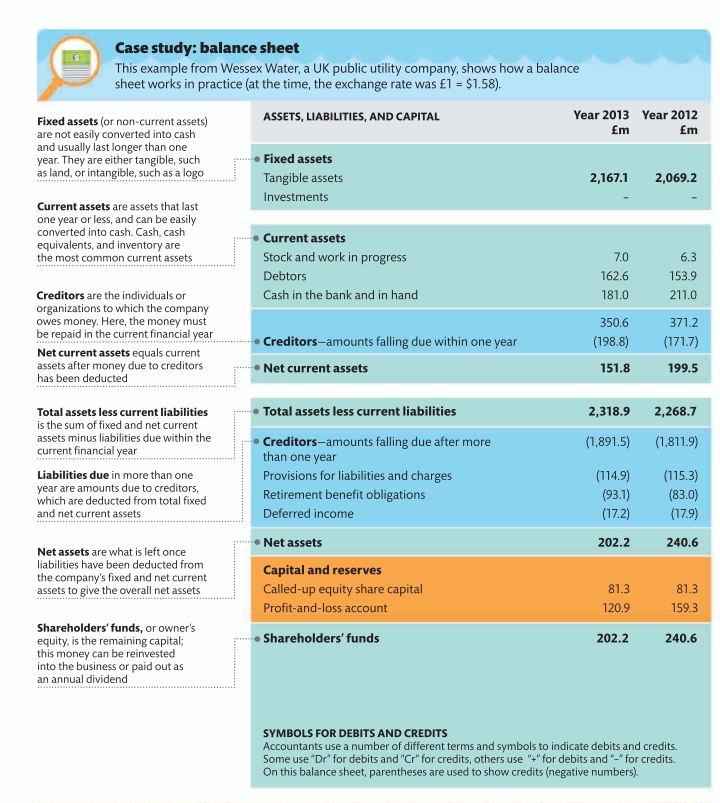

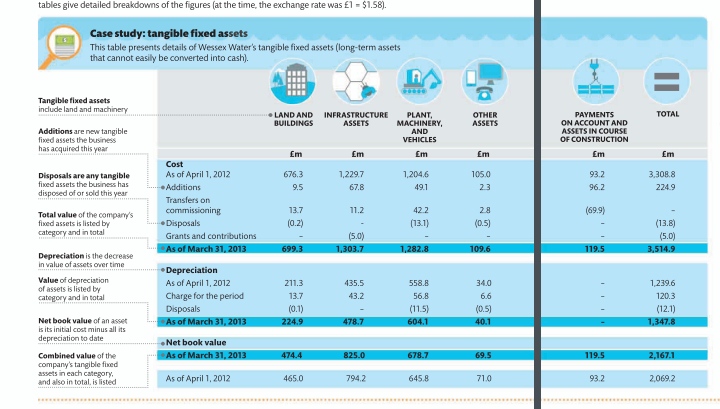

A balance sheet is a financial statement that shows what a business is worth at a specific point in time. Its primary purpose is to show assets, liabilities, and equity (capital), rather than financial results.

How it works