The money coming in and going out of a business is its cash flow; the balance of inflow and outflow is key to survival. Inflows arise from financing, operations, and investment, while outflows are expenses.

How it works

Cash flow is the movement of cash in and out of a business over a set period of time. Cash flows in from sales of goods and services, loans, capital investment, and other sources. Cash flows out to pay employees, rent and utilities, suppliers, and interest on loans. Timing is key—having enough cash coming in to pay bills on time keeps the company solvent.

Sales revenue

Cash for goods and services sold

- ❯ Revenue generated by core operation

- ❯ Basis of profit—does not have to be repaid, unlike loans or capital

- ❯ Company must be able to turn revenue into cash (get paid) to maintain cash flow

- ❯ Also known as cash flow from operating activities

Capital

Investment and lump sums

- ❯ Main source of cash inflow for start-ups

- ❯ Additional cash injection after initial start-up or at key stages in a company’s growt

- ❯Revenue from flotation of private companies (going public) and shares issued by public companies

- ❯ Also known as cash flow from investing activities

Loans

Bank loans and overdrafts

- ❯ Working capital loans to meet shortfalls, with anticipated inflows as collateral$ $CASH IN$ CASH OUT

- ❯ Advances on sales invoices from factoring companies

- ❯ Short-term overdrafts

- ❯ Also known as cash flow from financing activities

Other revenue

Grants, donations, and windfalls

- ❯ Grants from government or other institutions, usually one-time sums for research and development❯ Donations and gifts (applicable to nonprofit organizations)

- ❯ Sales of assets and investments

- ❯ Repayment of loans made to other organizations

- ❯ Tax refunds

“ Cash comes in, cash goes out, but the tank should never be empty.”

CASH OUT

Salaries and wages

Payments to employees

- ❯ Money paid to employees who are directly involved in the creation of goods or provision of services

- ❯ Salaries paid to staff as a fixed amount monthly or weekly (based on an annual rate)

- ❯ Wages paid to contractors for hours, days, or weeks worked

Overheads

Payment of bills

- ❯ Day-to-day running costs

- ❯ Rental cost of commercial property; utility bills—water, electricity, gas, telephone, and internet; office supplies and stationery

- ❯ Salaries and wages of employees not directly involved in creating goods and services (known as indirect labor)

Loan repayments

Debt servicing and shareholder profit

- ❯ Interest on long-term loans for asset purchases and on shortterm loans for working capital

- ❯ Repayments on capital loans

- ❯ Commission paid to factoring companies

- ❯ Cash distribution to shareholders via share repurchases and dividend payments

Suppliers

Payments for materials and services

- ❯ Cost of raw materials needed to manufacture goods for sale

- ❯ Cost of stock, imported or local

- ❯ Fees for services such as consulting or advertising to generate revenue

- ❯ Payments to contractors involved in goods and services creation

Tax

Payments to tax authorities

- ❯ Corporation tax based on annual financial statements

- ❯ Payroll tax paid by employers on behalf of employees

- ❯ Sales tax on goods or services

- ❯ Varies from country to country, depending on tax law

Equipment

Purchase of fixed assets

- ❯ Cost of buildings and equipment, such as computers and phones, office furniture, vehicles, plant, and machinery

- ❯ Offset by depreciation

Cash-flow management

The handling of cash flow determines the survival of any business. Equally important is a company’s ability to convert its earnings into cash, which is known as liquidity. No matter how profitable a business is, it may become insolvent if it cannot pay its bills on time. New businesses may become victims of their own success and fail through

“insolvency by overtrading” if, for example, they spend too much on expansion before payments start coming in and run out of cash to pay debts and liabilities. In order to manage cash flow, it is essential for companies to forecast cash inflows and outflows. Sales predictions and cash conversion rates are important. A schedule of when payments are due from customers, and when a business has to pay its own wages, bills, suppliers, debts, and other costs, can help to predict shortfalls. If cash flow is mismanaged, a business may have to pay out before receiving payment, leading to cash shortages. Some businesses, such as supermarkets, receive stock on credit but are paid in cash, generating a cash surplus.

WARNING

Top five cash-flow problems

- ❯ Slow payment of invoices

- ❯ Credit terms on sales invoices set at 60 or 120 days, while credit terms on outgoings are 30 days

- ❯ Decline in sales due to change in economic climate or competition, or product becoming outmoded

- ❯ Underpriced product, especially in start-ups trying to compete

- ❯ Excessive outlay on payroll and overheads; buying rather than renting assets

NEED TO KNOW

- ❯ Factoring Transaction in which a business passes its invoices a third party (factor), which collects payment from the customer for a commission

- ❯ Accounts payable Payments a business has to make to others

- ❯ Accounts receivable Payments a business is due to receive

- ❯ Aging schedule A table charting accounts payable and accounts receivable according to their dates

- ❯ Cash-flow gap Interval between payments made and received

Cash conversion

Successful businesses convert their

product or service into cash inflows before their bills are due. To make the conversion process more efficient, a business may speed up:

- ❯ Customer purchase ordering

- ❯ Order fulfillment and shipping

- ❯ Customer invoicing

- ❯ Accounts receivable collection period

- ❯ Payment and deposit

80%

of small business start-ups across the world fail because of poor cash-flow management

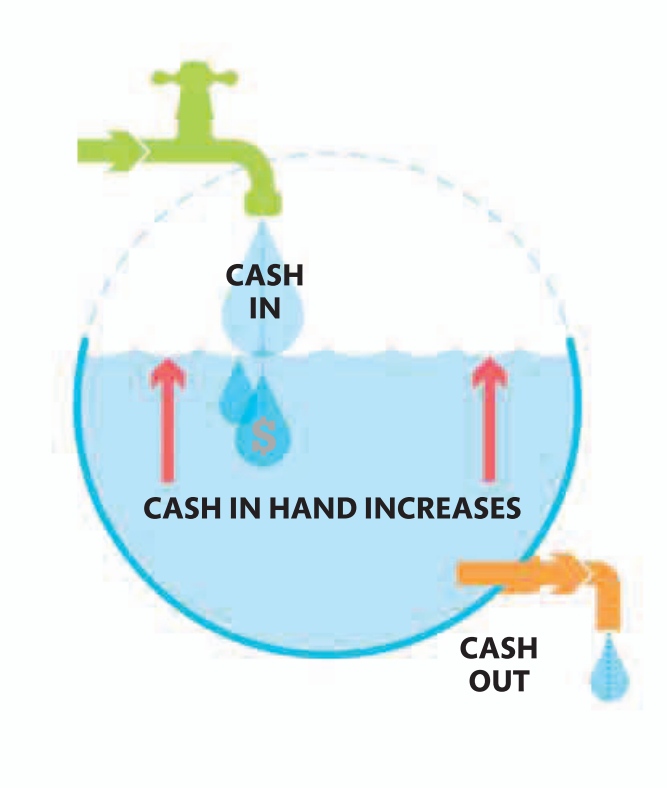

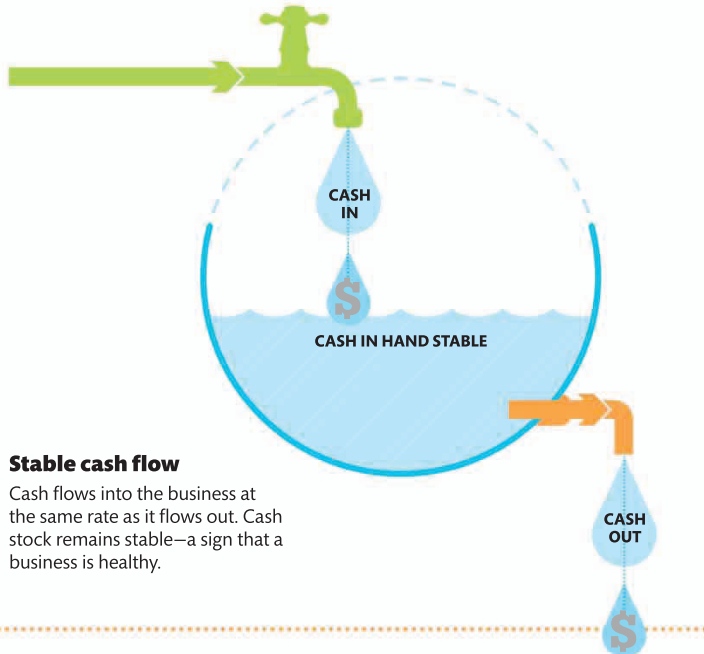

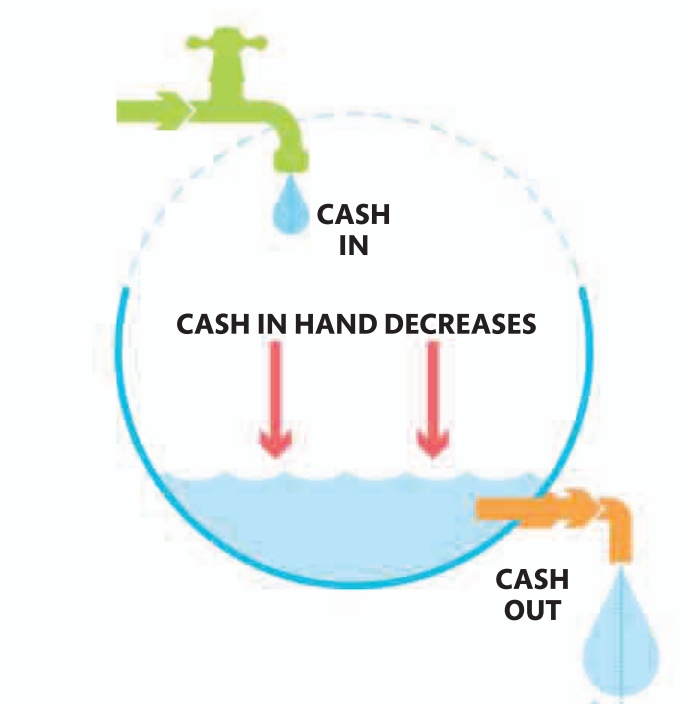

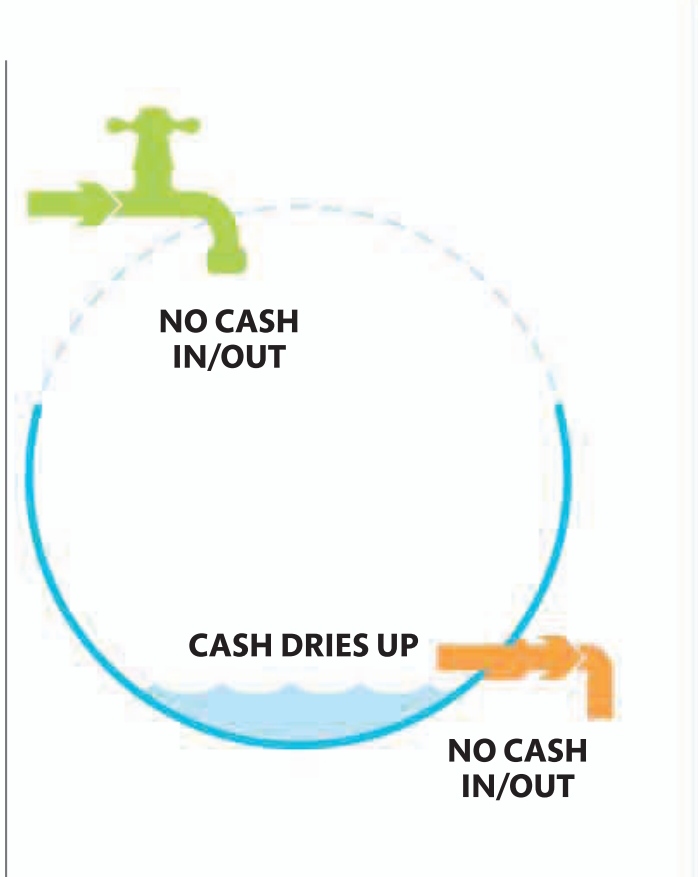

Positive and negative cash flow

Positive cash flow Cash flowing into the business is

greater than cash flowing out. Cash in the tank—stock—increases. A business in this position is thriving.

Stable cash flow Cash flows into the business at the same rate as it flows out. Cash stock remains stable—a sign that a business is healthy.

Negative cash flow Less cash is flowing into the business than is flowing out. Over time, the stock of cash will decrease and the business will face difficulties.

Bankruptcy If cash flowing out continues to exceed cash flowing in, cash stock levels will drop so low that the business becomes insolvent—it has no assets left to continue trading.

HANDLING THE FLOW

Managing a surplus

- ❯ Move excess cash into a bank account where it will earn interest, or make profitable investments.CASH IN

CASH IN HAND DECREASES

NO CASH IN/OUT - ❯Use cash to upgrade equipment to improve production efficiency.

- ❯ Expand the business by taking on new staff, developing products, or buying other companies.

- ❯ Pay creditors early to improve credit credentials, or pay down debt before it is due.

Managing a shortage

- ❯ Increase sales by lowering prices, or profit margins by raising them.

- ❯ Issue invoices promptly and pursue overdue payments.

- ❯ Ask suppliers to extend credit.

- ❯Offer discounts on sales invoices in return for faster payment.

- ❯ Use an overdraft or short-term loan to pay off pressing expenses.

- ❯ Continue to forecast cash flow and plan to avert future problems.

Leave a comment