The cash-flow statement shows the movement of cash during the last accounting period. It is important because it reveals a company’s liquidity—whether or not it has more money coming in than going out.

How it works The cash-flow statement is often more useful for investors assessing a business’s health than other key statements, because it shows how the core activities are performing. The profit-and-loss statement, for example, obscures this by adding in non-cash factors such as depreciation. Similarly, the balance sheet is more concerned with assets than liquidity.

How to read a cash-flow statement

The statement of cash flows, to give it its official title, answers the key question of whether a business is making enough money to sustain itself and provide surplus capital to grow in the future, pay any debts, and give out dividends. Figures in parentheses are negative numbers.

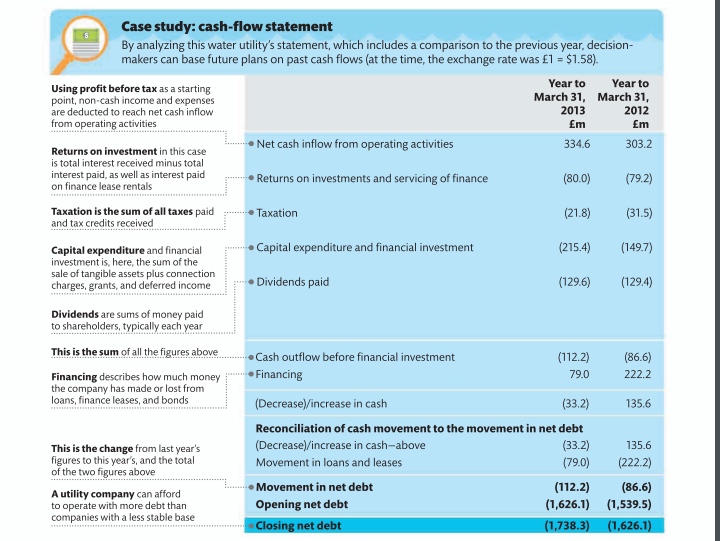

Case study: cash-flow statement

By analyzing this water utility’s statement, which includes a comparison to the previous year, decisionmakers can base future plans on past cash flows (at the time, the exchange rate was £1 = $1.58).

Three types of cash flow

Cash refers to actual money as well as cash equivalents including cash in the bank; bank lines of credit, and short-term, highly liquid investments for which there is little risk of a change in value. Cash does not include interest, depreciation, or bad debts (debts written off).

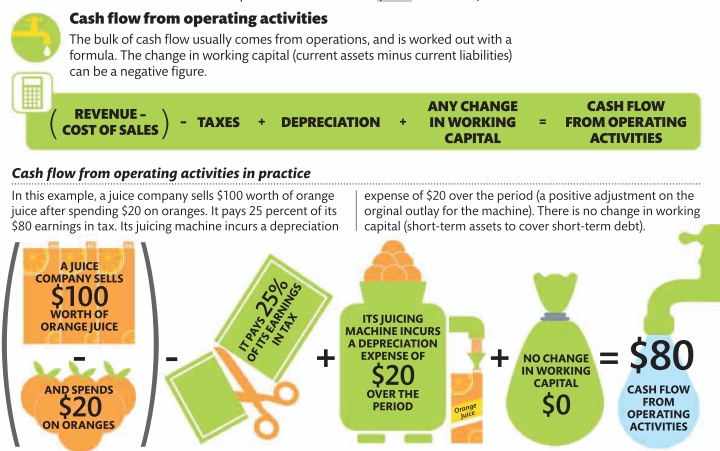

Cash flow from operating activities

The bulk of cash flow usually comes from operations, and is worked out with a formula. The change in working capital (current assets minus current liabilities) can be a negative figure.

Cash flow from investing activities

Buying or selling assets

or investments is in this category. This figure is usually a cash outflow (negative figure) due to buying more than selling, but can be positive if there are significant sales.

Cash flow from financing activities

This includes buying or

selling stock or debt and paying out dividends. Money made from selling something is called cash inflow; money lost through paying out is cash outflow.

Total cash flow

Adding all three cash flows gives the total. Separating

out the three types shows decisionmakers the health of core activities as opposed to financing and investing, which bear little relation to day-to-day operations.

Leave a comment