When a company buys an asset, its cost can be deducted from income for accounting and tax purposes. Depreciation allows the company to spread the cost, by calculating the asset’s decline in value over time.

How it works

If a business buys a long-lived asset, such as a building, factory equipment, or computer, to help it earn income, this expenditure can be offset as a cost against income earned. However, not all this income will be generated in the year of purchase and, over time, the asset will age and become less beneficial to the business, until it becomes outdated or unusable. Accountants do two things to

turn the declining value into a tax advantage. Firstly, they work out how much the asset’s value decreases over a period of time—typically a year. Secondly, they match that loss in value to the amount of income earned in that period, so depreciation becomes a deduction from taxable income. There are several different

ways to calculate depreciation. The method a company uses may depend on the kind of business, the type of asset, tax rules, or personal preference. In the United States, per IRS guidelines, companies must use MACRS (Modified Accelerated Cost Recovery System), a combination of straight-line and double declining balance methods.

NEED TO KNOW

- ❯ Fixed/tangible assets Items that enable a business to operate but are not a part of trade; assets lasting a year or more qualify for depreciation

- ❯ Useful/economic life Length of time an asset is fit for its purpose and has monetary value

- ❯ Salvage/scrap/residual value Worth of an asset once it has outlived its useful life—often set by the tax authority

- ❯ Book value An asset’s worth on

- paper at any point between its initial purchase and salvage

TYPICAL LIFE OF FIXED ASSETS

Tax authorities often specify the typical useful (economic) life of a particular asset. This helps to standardize depreciation, and to eliminate uncertainty about value and the number of years over which an asset can be depreciated.

60%

the value the average car loses after three years

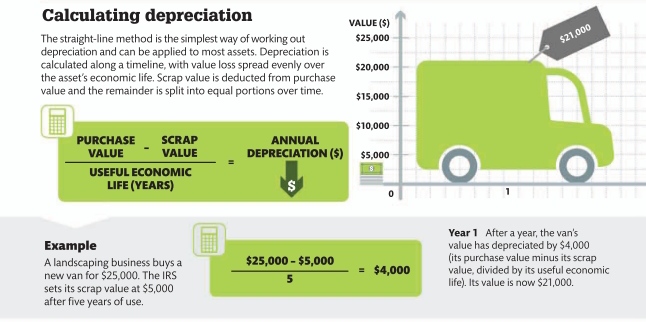

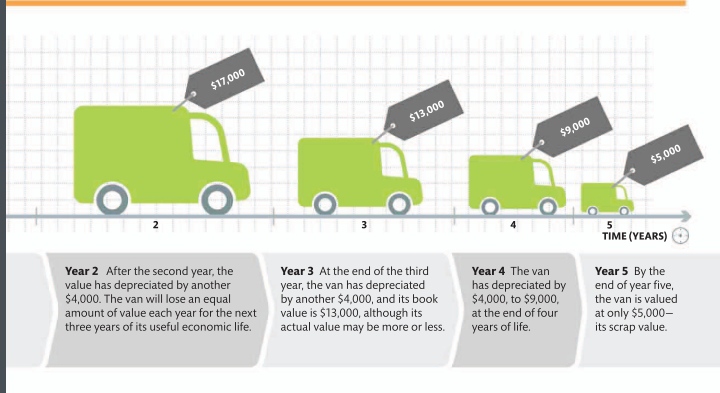

Calculating depreciation

The straight-line method is the simplest way of working out depreciation and can be applied to most assets. Depreciation is calculated along a timeline, with value loss spread evenly over the asset’s economic life. Scrap value is deducted from purchase value and the remainder is split into equal portions over time.

Applying depreciation

When calculating depreciation, there are a number of different factors to consider. For instance, a business needs to be able to predict the number of years an asset will last. Helpfully, tax authorities in most countries issue guidelines to accountants and businesses with estimates of the useful economic life of many common business assets. Companies may also wonder

which of the many methods of calculating depreciation to use for a given asset. Each method reflects a different pattern of depreciation, with some being more suitable for particular categories of assets. For example, the “accelerated” methods that chart rapid depreciation at the beginning of an asset’s life are more suitable for technology, while the “activity” methods that link depreciation to actual hours of use or number of units produced are best suited to transport and production lines. Again, tax authorities in most

countries offer guidelines on which method to use. Although it is technically possible for a company to use two different methods for their own accounting and for tax purposes, this is best avoided.

WARNING

Misusing depreciation

- ❯ The wrong method A company must choose a method that is permissible for an asset type

- ❯ Frontloading Opting for an accelerated method can result in a taxable gain if an asset is sold early, for more than its book value

- ❯ Claiming beyond useful life Depreciation cannot be claimed after an asset’s useful life

- ❯ Ignoring depreciation If a company fails to claim depreciation, it has to report a gain from the sale, despite the loss on deduction

Other depreciation methods

There are many different methods of calculating depreciation. Some are favored by particular tax codes, while others are specifically applicable to certain industries and types of assets, and their patterns of value loss.

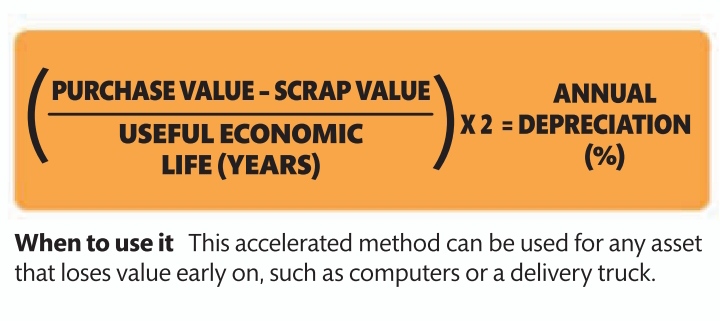

Double declining balance method

A method used to claim more depreciation in the first years after purchase, which is useful for

assets that lose most of their value early on. It reduces a company’s net income in the early years of an asset’s life, but generates initial tax savings.

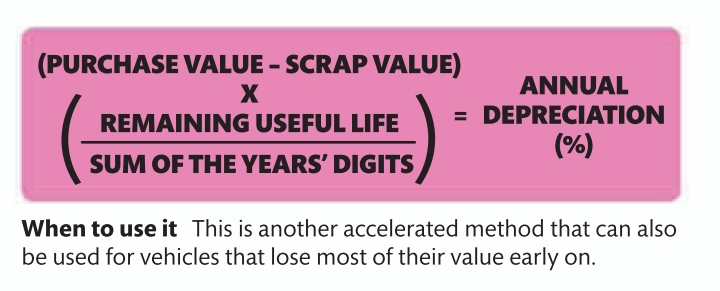

Sum of the years’ digits method (SYD)

Depreciation is calculated by dividing each

year of the asset’s life by the sum of the total years to give a percentage of the depreciable value. If the asset’s useful life is 5 years, then the sum of the years as digits is 15 (5 + 4 + 3 + 2 + 1). In year 1, it loses 33 percent (5 ÷ 15), in year 2, 27 percent (4 ÷ 15), and so on.

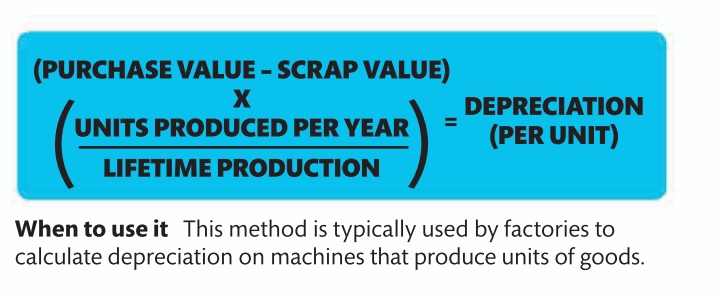

Units of production method

When a company uses an asset to produce quantifiable units, such as pages printed

by a photocopier, it can claim depreciation with this method, which calculates depreciation according to the number of units an asset produces in a year.

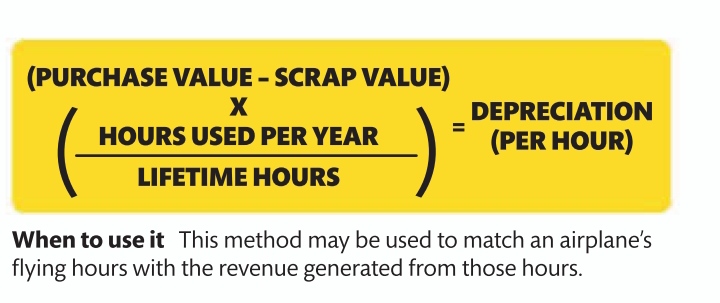

Hours of service method

The asset’s decline in value is measured according to the number of actual hours it is

in use. To calculate depreciation using this method, the company measures the hours of use per year as a percentage of the estimated total lifetime hours. It is particularly useful for transportation industries.

Leave a comment