Almost every new enterprise needs funding to get it going, and to keep afloat until it turns a profit. Financial help is at hand from a variety of sources, suitable at different stages of start-up growth.

How it works

Capital for new enterprises comes from two main sources: lenders and investors. Lenders, such as banks, provide debt capital in the form of a loan that is returned with interest. Investors, such as business angels and venture capitalists (VCs), provide equity capital in the form of a share in the business that may include a proportionate share of control and rewards. Both types of funding can be corporate—from a company—or more quirky and alternative, such as crowdfunding.

Types of start-up funding

Corporate, traditional, and substantial funding comes largely from banks and VCs, while smaller sums come from more personal sources.

- Lenders

- Investors

- Grants

Lenders

Debt capital most often takes the form of loans paid back with interest.

Term loan Paid back regularly over a set period of time

❯ Bank Offers either personal or business loans

❯ Government Offers low-interest start-up loans

❯ Credit union Cooperative that gives members low-interest loans

❯ Peer-to-peer (P2P) lending Unsecured personal loans

❯ Friends and family May give interest-free loans

Bank overdraft or credit card Interest charged monthly if balance not paid in full

❯ Bank or credit company Financial organization that makes loans to commercial ventures

Factoring/invoice discounting Unpaid invoices sold at a discount to a company that collects them for commission

❯ Factors and discounters Companies that offer advance on unpaid invoices, for a profit

Investors

Equity capital is paid to the start-up in return for a share of the business.

Founders, friends, family (FFF) May buy shares in the company rather than lending money

Crowdfunding Large number of supporters, each contributing a small amount of money, usually online

Business angels Investors who give favorable terms because their focus is on the company’s success rather than profit

Venture capitalists (VCs) Companies that provide capital for new businesses in the hope of making a profit

Grants

Financial awards and prizes are provided by public bodies.

Local, national, global Funded by a local authority, government initiative, or international charity

NEED TO KNOW

❯ P2P lending Loans made between individuals over internet

❯ Crowdfunding Debt or equity raised via internet platforms

SUPER ANGELS

❯ What they are Serious investors in technology start-ups. Facebook was funded by super angels, some of whom are now famous in their own right.

❯ Who they are Former Silicon Valley professionals who invest their personal money in new ventures.

❯ How they differ from ordinary angels and venture capitalists (VCs) Funding level straddles the two, often reaching millions of dollars as what started out as a hobby becomes a profession.

❯ Pros and cons Super-angel investing acts like a magnet to other investors, but individual super angels can rarely provide the full funding of a VC.

Alternative models

Since the start of the economic downturn that started in 2008, several innovative and more personal types of funding, such as crowdfunding and peer-to-peer (P2P) lending, have evolved and blossomed on the internet. All involve the principle of raising small amounts of money from large numbers of individuals who pool their resources to provide the loan or equity needed.

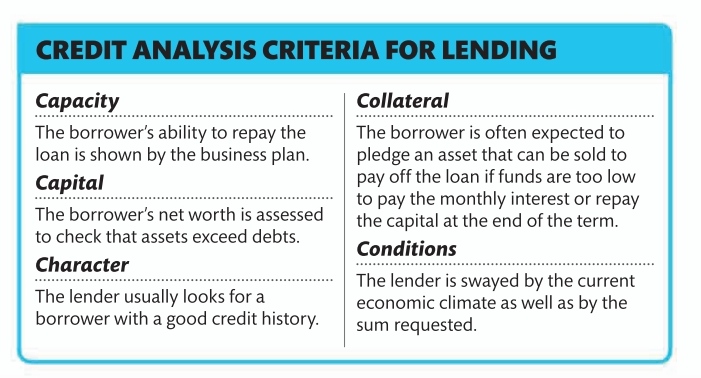

CREDIT ANALYSIS CRITERIA FOR LENDING

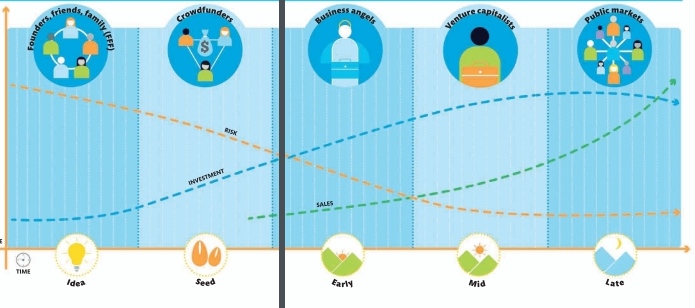

Life cycle of investment

The key to successful funding is to choose the right type of finance at each stage of a company’s early growth. Start-ups usually begin modestly, with self-funding and help from friends, family, and anyone else who is prepared to take a high risk. Crowdfunders and business angels are amateurs willing the entrepreneur to succeed, while venture capitalists become interested when the level of risk goes down and they can expect a healthy profit in return for injecting substantial funds. Public markets such as stock exchanges may step in as sales soar and success looks probable. At all stages, investors will conduct credit analyis to asses a company’s ability to repay its debt.

5–10%

of small and medium-sized enterprises in the UK need no start-up funding

Leave a comment